3 reasons why today’s Fed rate cut is the beginning of a more aggressive cutting spree than investors expect: chief economist

Federal Reserve Bank Chair Jerome Powell

The Federal Reserve is expected to slash interest rates today for the first time since 2020 as the labor market and inflation continue to cool.

The move is widely anticipated among investors after Jerome Powell’s dovish speech in Jackson Hole, Wyoming, in August. What the market is wrongly forecasting, however, is just how aggressive the Fed’s rate-cutting campaign will be over the next several months.

That’s according to Pantheon Macroeconomics Chief US Economist Samuel Tombs. Current market odds favor the central bank cutting rates by 225 basis points to the 3%-to-3.25% range by June or July 2025, according to the CME FedWatch tool. But Tombs said in a note to clients on Monday that the Fed will have dropped rates even further by that point, to 2.5%-2.75%.

“We think the Fed will have to be more proactive than it will envisage this week and eventually will reduce the funds rate to 2.625% by mid-2025,” he wrote.

Assuming a 25-basis-point cut at every FOMC meeting until next July, that would leave an extra 75 basis points the central bank would have to work into its policy adjustments over that time.

There are a few reasons Tombs thinks the oncoming cutting cycle will be more frantic than many anticipate. One is that the consumer could be weaker than they appear, and the labor market is likely to deteriorate further.

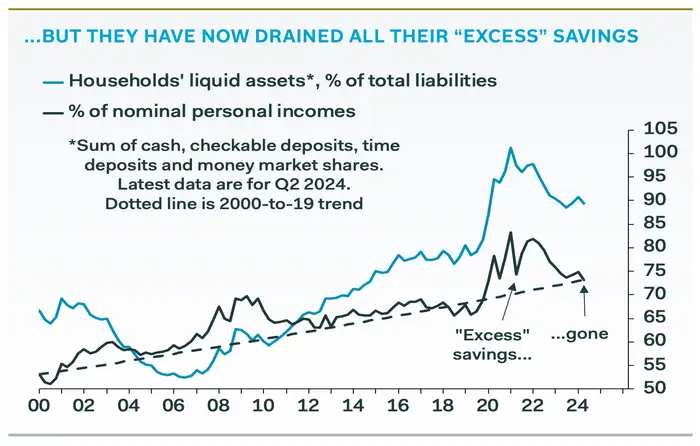

While household balance sheets are strong thanks to home price growth and record stock prices, excess pandemic savings from government stimulus and reduced consumption have dried up, Tombs said. This is evident in cash levels as a percentage of income returning to where they would normally be expected to be by now by 2019 standards.

This suggests consumers’ firepower may be stalling, and a rising unemployment rate will only worsen this. With NFIB data showing falling hiring intentions and job openings on the decline, Tombs thinks unemployment will continue its upward trend. When the job market worsens, people tend to save more money.

While the Fed hopes to stimulate spending with rate cuts, Tombs is skeptical that they’ll the impact the central bank wants.

Because of a weaker consumer and a labor market trending the wrong way, a majority of banks are growing more wary of giving out loans, Tombs pointed out. That’s likely to keep rates high in the near-term.

“Lenders are rightly pricing in higher default risk,” Tombs wrote.

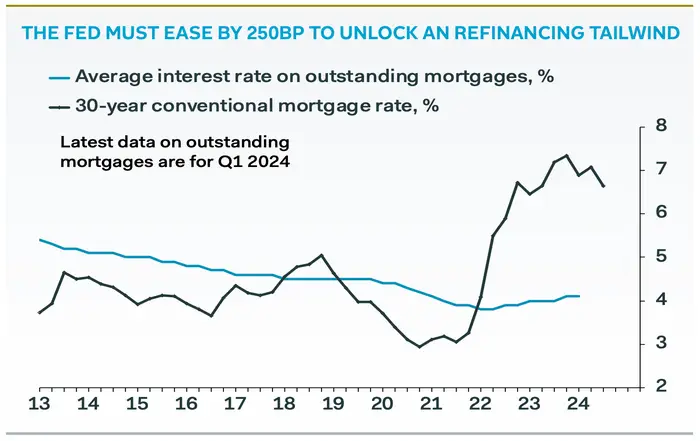

Mortgage rates would also need to come down significantly to benefit the many homeowners who already have low mortgage rates locked in, Tombs said, and lower rates will hurt returns on assets like certificates of deposits and money market funds.

“New mortgage rates need to drop by about 250bp before they will undershoot the average outstanding mortgage rate,” Tombs wrote. “Indeed, Fed easing probably will depress households’ cashflow initially, given that liquid assets now stand at 90% of liabilities, up from 60% in the 2000s, and the effective interest rate on deposits will fall more quickly than the effective loan rate.”