4 charts Goldman Sachs is watching as it predicts an era of weak stock returns ahead

The stock market’s benchmark index is poised for a decade of tepid returns, Goldman Sachs predicted this month.

The investment bank said it sees a decade of weak gains coming for the S&P 500, thanks to a confluence of factors, such as a weakening economy, high market concentration, and an unfavorable backdrop in Treasury yields.

Those headwinds could lead the benchmark index to return just 3% in nominal annualized returns for the next 10 years, strategists said, down from the S&P 500’s average 13% annualized return over the last decade.

Here are four charts the bank is watching as it sees the S&P 500’s golden era for stocks winding down.

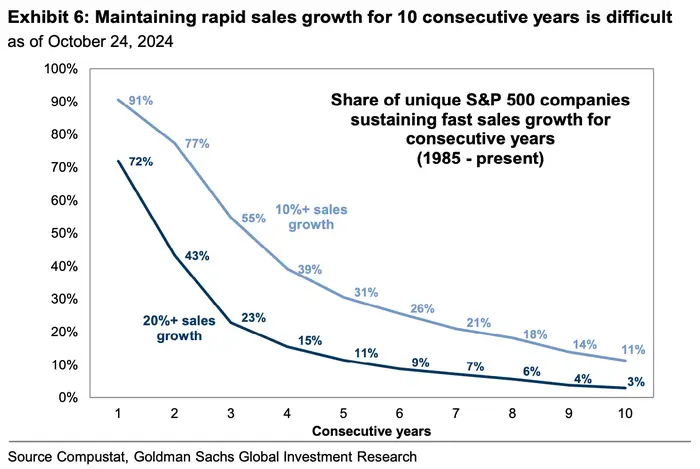

1.Only a few S&P 500 companies are sustaining sales growth

The percentage of unique S&P 500 firms that have maintained high sales growth is small.

The share of companies that maintained 10% or higher sales growth for 10 years is 11%, while the share of companies that maintained 20% or higher sales growth for 10 years is 3%, according to the firm’s analysis of corporate earnings dating back to 1985.

Just 3% of unique S&P 500 companies have maintained 20%+ sales growth for 10 years, per Goldman’s analysis.

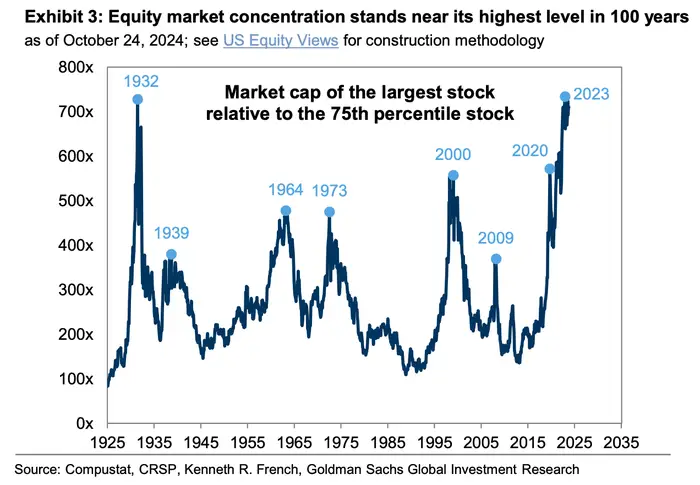

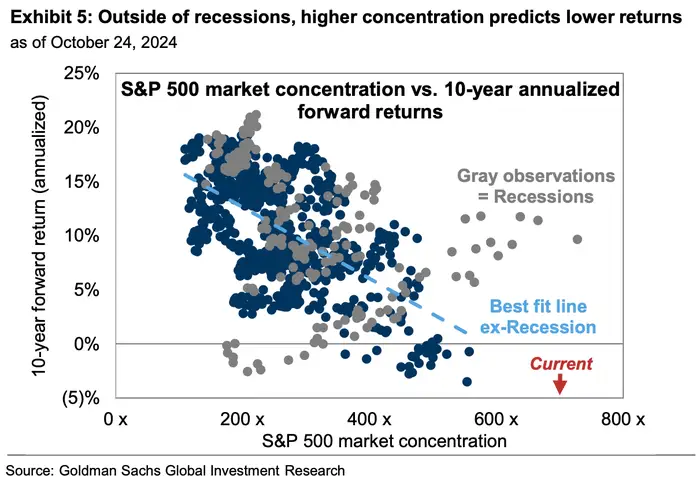

2.S&P 500 market concentration is at its highest levels in a century

The largest stock in the S&P 500 is has a market cap over 700 times the market cap of the index’s 75th percentile stock. That’s the highest multiplier seen in about 100 years, a sign the benchmark index is highly concentrated.

The S&P 500 was the most concentrated last year since 1932.

Higher market concentrations have typically led to poorer returns for the S&P 500 over the next 10 years, barring recessionary periods.

Outside of recessionary years, S&P 500 returns over the following decade tend to be poorer when market concentration is higher.

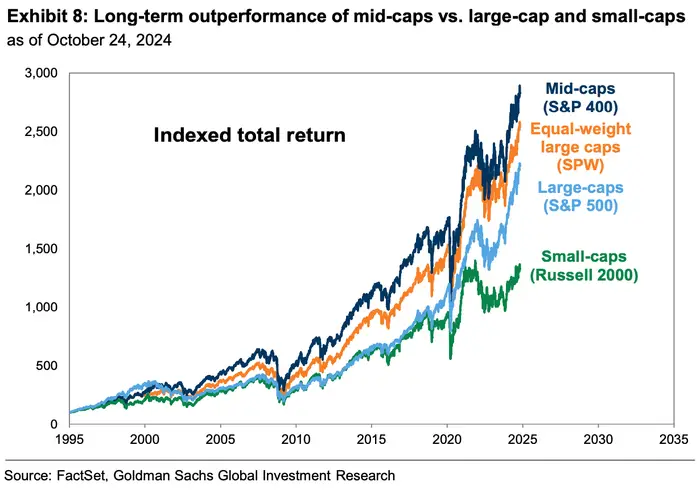

3. The S&P 500 is seeing relative underperformance

Total returns for the S&P 500 since the start of the year have fallen behind several other assets, indexes, and individual sectors, including the Russell 1000, bitcoin, and gold.

Meanwhile, the total return of the S&P 500 has trailed behind the SPW, an equal-weight index of large-cap shares, and the S&P 400, an index of mid-cap stocks, for years.

The total return of the S&P 500 has fallen behind the S&P 400 and the SPW, Goldman’s analysis found.

“Investors should consider allocating to other indices where we view the current landscape as favorable for strong forward performance,” strategists said, highlighting in particular the equal-weight S&P 500 and the mid-cap S&P 400 index.

“Long-term performance of these alternatives reflects the fact that the strength of the US economy and the earnings and innovative capacity of US corporates can be captured outside of large-cap and capitalization-weighted indices.”

The S&P 500 is up 23% year-to-date, and corporate earnings have been relatively strong so far this quarter. According to FactSet, 75% of the companies that have reported earnings have beat earnings estimates, on par with the 10-year average.

Goldman Sachs strategists said they’re bullish on the S&P 500 over the short term, forecasting 8% growth in earnings per share by the end of 2024 and 11% EPS growth the following year.

The benchmark index is on track to hit 6,300 over the next 12 months, the strategists predicted, implying another 8% upside from current levels.