A notorious market bear who called the 2000 and 2008 crashes warns stocks are in their ‘third great speculative bubble’ in the last 100 years

A trader blows a chewing gum bubble as he works on the floor of the New York Stock Exchange shortly after the opening bell, in New York, June 15, 2015.

John Hussman, the president of the Hussman Investment Trust who called the 2000 and 2008 market crashes, isn’t shy about his characterization of the current market environment.

“I continue to view [the] period since January 2022 as the extended top formation of the third great speculative bubble in US financial history,” he wrote in a September 23 note — the other two bubbles being in 1929 and 1999.

It’s a bold call, especially considering that a majority of investors and economists believe a soft-landing is likely as the Fed begins to reduce rates. It’s also a bold call with stocks at fresh record highs, the S&P 500 up almost 60% since October 2022 lows, thanks largely to excitement around artificial intelligence. The rally has been so unrelenting it’s changed the minds of top Wall Street bears like Mike Wilson and Michael Kantrowitz along the way.

To paraphrase Lance Armstrong, the former Tour de France champion later caught for doping, extraordinary accusations require extraordinary proof.

Hussman believes he has sufficient proof for his striking assertion. But that’s for investors to decide.

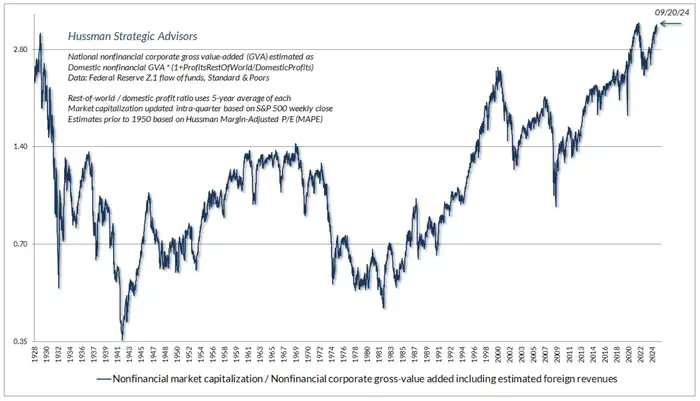

The first piece of evidence Hussman cites is valuation, specifically the total market cap of non-financial stocks to total value added of those stocks. His favorite and most reliable valuation metric for determining long-term market returns has climbed to just below the all-time-highs seen in 2022, and hovers above levels reached in 2000 and 1929.

While valuations are indeed at nosebleed levels, they can be of little help to investors in determining near-term returns. Plus, if rates are set to come down and the economy flourishes without reigniting inflation, who’s to say valuations and stock prices can’t climb higher?

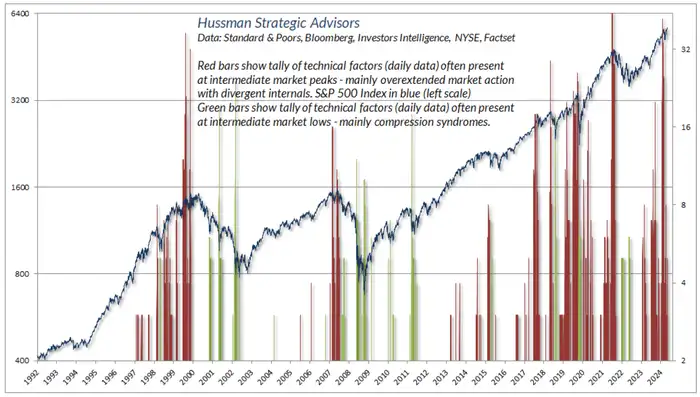

But Hussman has technical data like breadth indicators that show stocks could be ripe for a decline — though he distances himself from making such a prediction. Through the years, Hussman has identified various technical behaviors around market peaks and market troughs, and on September 20 and July 16, the sum of warning indicators flashing red surged to levels seen only leading up to 2000 and 2022.

When the tally of negative signs has risen to 16 (shown on the right side of the chart below) or above over the last few decades, the S&P 500 has seemed to undergo a correction shortly after.

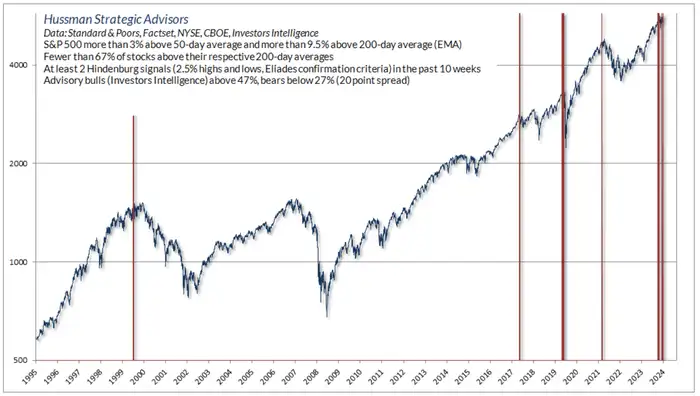

Here’s one of those factors included in the tally above. Its parameters are: the S&P 500 is at least 9.5% above its 200-day moving average and at least 3% above its 50-day moving average; less than one-third of stocks in the S&P 500 are above their 200-day moving averages; at least 2.5% of S&P 500 stocks are at new highs while at least 2.5% are at new lows; and bullish investors outweigh bearish investors by at least 20%, going by Investors Intelligence data.

The factor was present right before major declines in 2022, 2020, and 2000, as well as a minor decline in 2017.

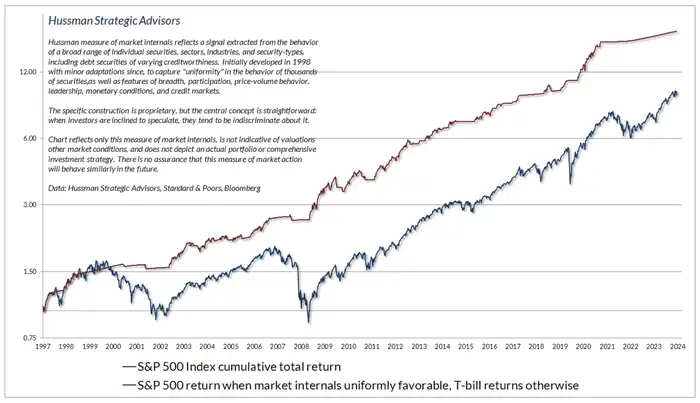

Hussman’s metric of “market internals,” essentially a measure of overall market breadth that acts as a gauge on investor sentiment, is also showing poor readings (when the line is relatively flat), which usually correspond with market drops. The last time the metric went this flat for this long was during the dot-com bubble.

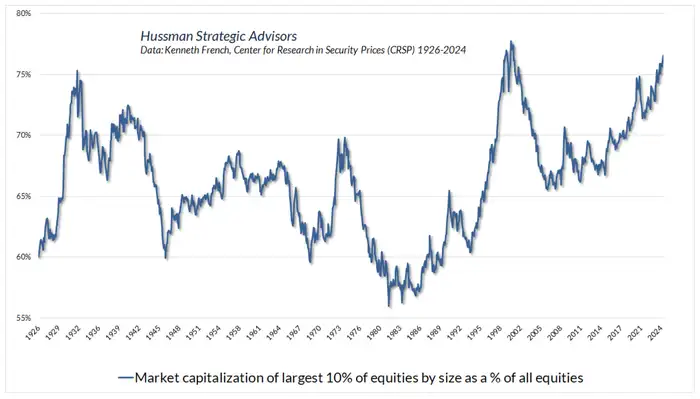

Finally, Hussman pointed to the high concentration levels in the market. The top 10% of all US stocks by market cap make up around 76% of the market’s total capitalization. The only two times it has crossed 75% was around 2000 and 1929.

Hussman’s track record — and his views in context

To go back to the Armstrong reference, one might view Hussman as playing a similar role to Irish journalist David Walsh, one of the reporters who brought the cyclist’s doping practices to light after years of digging. The market continues its winning streak while Hussman continues to argue that the rally isn’t quite what it looks like, and the truth will come out.

The only problem with that analogy is we don’t know yet whether the market turns out to be Armstrong or not.

Labor market data is softening, causing recession concerns to surface. If a downturn does arise, it would catch investors off guard, and likely sink the market.

But if the Fed can nail the soft landing and the unemployment rate stabilizes in the months ahead, investors may continue to enjoy the stellar returns they’ve seen over the last couple of years. Higher potential profit margins from AI could also fuel the rally further.

For the uninitiated, Hussman has repeatedly made headlines by predicting a stock-market decline exceeding 60% and forecasting a full decade of negative equity returns. And as the stock market ground mostly higher, he persisted with his doomsday calls.

But before you dismiss Hussman as a wonky perma-bear, consider again his track record. Here are the arguments he’s laid out:

- He predicted in March 2000 that tech stocks would plunge 83%, then the tech-heavy Nasdaq 100 index lost an “improbably precise” 83% during a period from 2000 to 2002.

- He predicted in 2000 that the S&P 500 would likely see negative total returns over the following decade, which it did.

- He predicted in April 2007 that the S&P 500 could lose 40%, then it lost 55% in the subsequent collapse from 2007 to 2009.

However, Hussman’s recent returns have been less than stellar. His Strategic Growth Fund is down about 54% since December 2010, and has fallen 14% in the last 12 months. The S&P 500, by comparison, is up about 32% over the past year.

The amount of bearish evidence being unearthed by Hussman continues to mount, and his calls over the last couple of years for a substantial sell-off began to prove accurate in 2022. Yes, there may still be returns to be realized in this new bull market, but at what point does the mounting risk of a larger crash become too unbearable?

That’s a question investors will have to answer themselves — and one that Hussman will keep exploring in the interim.