Jeremy Grantham’s right-hand man Ben Inker warns your 60/40 portfolio is in for a ‘lost decade’ of negative returns

For decades, the 60/40 strategy has been the gold standard of investing.

Financial advisors often recommend allocating 60% of your portfolio to stocks and 40% to bonds — the S&P 500 and Bloomberg US Aggregate Bond Index being specific benchmarks. The 60% concentration in equities provides broad economic exposure and long-term capital appreciation, and the 40% concentration in bonds offers diversification and reduced volatility.

Since 1979, this investment breakdown has yielded over 10% returns annually.

It’s intuitive, passive, and generates returns — the perfect strategy for an investor looking to grow their portfolio without taking on too much risk.

There’s just one problem, according to Ben Inker, the cohead of asset allocation at GMO, the firm cofounded by investing legend Jeremy Grantham: sometimes the strategy doesn’t actually perform well at all.

Upon second glance, hidden within the 60/40 strategy’s impressive history of returns are six periods, spanning an average of 11 years each, when the portfolio actually yielded flat or negative real returns.

According to Inker, the strategy is due for another “lost decade” of poor returns.

One similarity that Inker sees between today and previous “lost decades” is that they came on the heels of periods of robust 60/40 portfolio returns, beginning when stocks or bonds were trading at elevated valuations. Since 2009, the stock market has benefited tremendously from loose monetary policy, and many equities today are trading at expensive multiples.

Inker is also skeptical because the performance of the S&P 500 is disproportionately driven by the companies with the biggest market capitalizations, and the Bloomberg US Aggregate Bond Index is overexposed to borrowers who issue the most debt, he said. Passively contributing money to these indexes leaves one vulnerable to the whims of investors and their feelings about the market, he said.

As a result, the 60/40 portfolio right now is not set up to generate attractive returns. In fact, in the near term, it’ll likely end up delivering low single-digit gains — or even worse, negative returns — in Inker’s view.

Investing against the grain

Instead of the traditional 60/40 portfolio, Inker recommends taking a more flexible approach to different asset allocations.

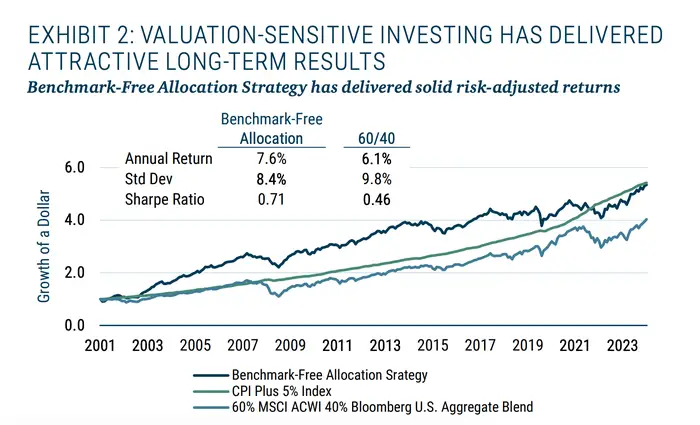

GMO’s Benchmark Free Allocation Strategy, which is actively rebalanced to take advantage of undervalued opportunities in the market, has outperformed the 60/40 portfolio on a risk-adjusted basis for the last two decades. The benchmark-free strategy returned 7.6% annually while a 60/40 portfolio returned 6.1% over the same period.

Right now, GMO’s benchmark-free portfolio is split into 53% equities, 30% alternative strategies, and 17% fixed income.

Within those categories, Inker highlights a few especially promising investment opportunities.

Look for value outside of the US with international equities, he said. While US equities have solid fundamentals, they’ve become extremely expensive. According to Inker, US equity valuations are at or approaching their highest price premium compared to the rest of the world. US P/E ratios are trading at a whopping 50% premium to historic averages.

International stocks, on the other hand, are trading below their historic averages. And with the dollar priced strongly against international currencies, investors will see their money go further in overseas markets. Inker is especially bullish on Japanese equities, which he believes will receive a boost from corporate governance reforms and cheap currency.

Within the US, deep value, or the cheapest 20% of the market, is trading at record lows. Inker believes the historic discrepancy between deep value and the rest of the market is a tailwind for these cheap stocks to appreciate and outperform.

Growth names are also trading at historic highs relative to value. Among the top 1,000 US stocks, the most expensive 20% of the market is trading at an 89th percentile premium compared to history.

Valuation gaps in the market have historically reverted to the mean, according to Inker.