A 33-year-old self-made millionaire shares the 2-part ‘financial freedom road map’ that helped him build wealth

Financially independent stock trader Erik Smolinski and his wife Mel.

Erik Smolinski got a head start on investing: In high school, a teacher encouraged him to put the money he was earning from odd jobs into the stock market.

He went to the library, picked up a couple of books, and started learning about basic investing concepts. From there, he started buying stocks.

In college, he continued working various jobs to fund his investment account, including flipping beaten-down cars with a buddy.

After graduating, he served in the Marine Corps and continued trading. As of 2024, the 33-year-old considers himself financially independent and has a seven-figure net worth, which B-17 verified by looking at screenshots of his trading account.

Smolinski, who trades full-time and creates investment content on YouTube, is adamant that “there are a handful of core concepts that if just about anybody can get their arms around, they can essentially hit most financial goals, especially if you start early enough.”

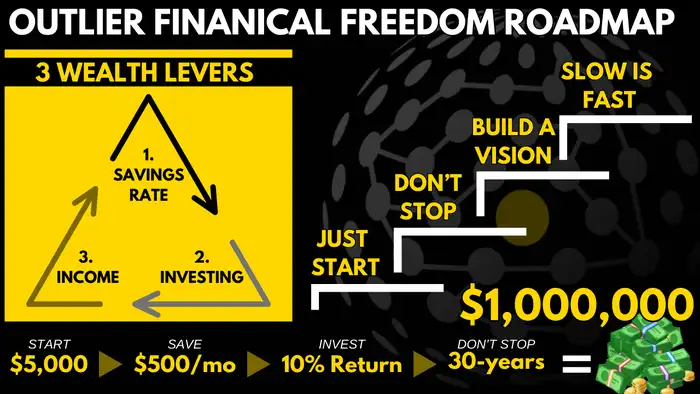

He created a two-part “financial freedom road map” to illustrate the core concepts.

Part 1: Understand 3 ‘wealth levers’

According to Smolinski, there are three “wealth levers” that you have to use in order to build wealth.

1. Savings rate. You can’t start building wealth without keeping at least a portion of your income.

Don’t “wait until you have more,” emphasized Smolinksi. Start saving whatever you can, even if it’s as little as $10 a month. The key is to form the habit.

2. Investing. Now that you have a chunk of savings, don’t just keep it in a bank account where it’ll earn little to zero interest.

After all, “You can’t save your way to wealth,” he said. “You can save your way to financial security, but if we’re talking about wealth, simply saving your entire life is not going to get you there. The investing component is what begins the compounding clock — and the sooner, the better.”

3. Income. The third lever can increase your overall savings rate, free up more money to invest, and ultimately speed up the wealth-building process. An extra $100 that you can contribute to an investment account on a monthly basis “can massively change the picture for you,” said Smolinski.

In terms of pulling on this lever, you have two main options: Pursue promotions and raises within your 9-to-5 or start a side hustle.

“If I’m working a corporate job with the idea of trying to make as much money as I can, one of the things I have to keep in mind is, for a lot of jobs, I’m going make more money if I job switch every two or three years or so,” he noted. Know your value and don’t hesitate to shop around.

“If you have a career that is not supremely time demanding and you have some space to do other stuff, you have to do it ethically because different jobs have different rules in terms of what kind of side hustles you can pick up, but pick up a side hustle,” he said. “Go drive Uber, go drive Doordash, go do something.”

Part 2: Take action in 3 steps

Keeping the wealth levers in mind, here are three steps Smolinski took that anyone can replicate to hit their money goals.

1. Just start: Open a brokerage account and contribute what you can

To pull on the second wealth lever, you’ll need a place to invest your money. A simple solution is to open a brokerage account.

“Any reputable broker is fine. Google search ‘top brokerage accounts,’ maybe watch a YouTube video where somebody compares them, and pick one that you like,” said Smolinski. Next, link your bank account to your brokerage account and initiate your first transfer. “Move money over — $25, $50, $100 — whatever you can possibly move over at that exact point, do it.”

You’ll want to spend some time thinking about how to invest your money. While Smolinski is an active trader, experts typically recommend that the everyday investor should stick with passive investing as a long-term, wealth-building strategy. Smolinski agrees: “I genuinely believe for the vast majority of people that’s probably the right answer.”

With passive investing, the goal is to match, not beat, the market. While it likely will not result in big short-term gains, it’s lower-risk and less volatile than active investing. One of the most popular passive investing approaches is to buy index funds.

Note that you can also invest in diverse funds in retirement-specific accounts like IRAs and 401(k) plans, which offer excellent tax advantages and, therefore, have annual contribution limits.

2. Don’t stop: Invest consistently

Now that you’ve started the process of investing your money and taking advantage of compound interest, “maintain the momentum,” said Smolinski.

The simplest way to force yourself to invest consistently is to set up automatic contributions. Over time, you’ll learn to live without the chunk of money you’re setting aside for your future.

“It gets real when you’re moving money away from yourself. It’s weird in the beginning because you’re sacrificing the ability to use that money for some sort of near-term gratification,” he noted, but that’s where step three comes in.

3. Build a vision

Saving aggressively to invest the excess will be easier if you have a specific goal, such as early retirement or buying your first home.

Smolinski’s goal was to become a millionaire by 30. He says he did some reverse engineering using an Excel spreadsheet: “I looked at different scenarios and I said, ‘OK, if I save this much, starting with this much money at these different returns, this is how much I’ll have in five years, this is how much I’ll have in 10 years.'”

It helped him visualize just how significant an extra couple hundred dollars a month could be, which changed his spending habits.

“When I was making these near-term trade-offs, it was always in the context of, ‘OK, if I go out, I’m going to grab dinner, I’m going to have drinks, that’ll probably be about 100 bucks. That 100 bucks can get me through this entire month for what I’m supposed to save,'” he said. “And then what ends up happening as you get into this mindset is that it starts to become addictive. You’re like, ‘If I do $100 a month, it gets me here. What if I actually did $200? How much faster could I get to where I’m trying to go?'”

The last step on Smolinski’s wealth-building ladder is “slow is fast,” he added. “By starting slow and building the habit, you’ll get to your end destination light years faster than you probably would ever expect.”