The S&P 500’s golden decade of returns is over, Goldman says

The stock market’s decade-long golden age will soon be a thing of the past, says Goldman Sachs.

A new report from the firm’s portfolio strategy research team forecasted that the S&P 500 will see an annualized nominal return of 3% over the next 10 years. That would put it in the 7th percentile of performance since 1930. It would also badly lag the 13% annualized figure put up by the benchmark index over the prior decade, Goldman data show.

“Investors should be prepared for equity returns during the next decade that are towards the lower end of their typical performance distribution relative to bonds and inflation,” the analysts wrote.

As an extension of this forecast, Goldman also sees stocks struggling to outperform other assets over the next 10 years. By its calculation, the S&P 500 has about a 72% chance of trailing bonds, and a 33% probability of lagging inflation through 2034.

Five factors underline Goldman’s lackluster outlook:

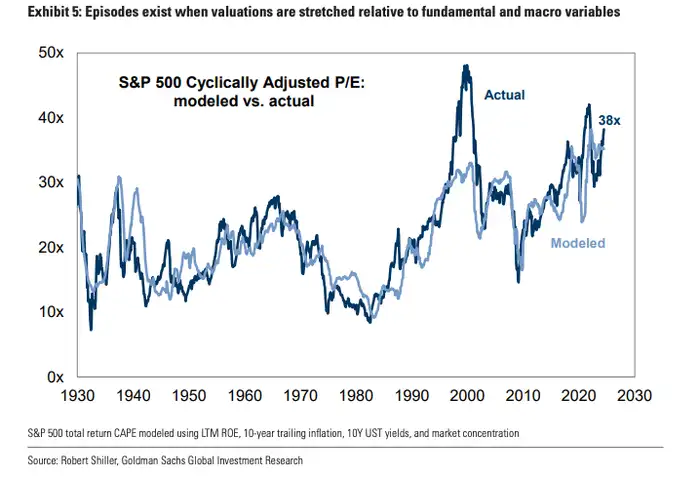

First, a historically stretched stock market valuation implies lower future returns, the bank said. Current valuations are indeed elevated, with the cyclically adjusted price-earnings ratio currently at 38 times, or in the 97th percentile.

The S&P’s 500 CAPE has averaged 22%, Goldman noted.

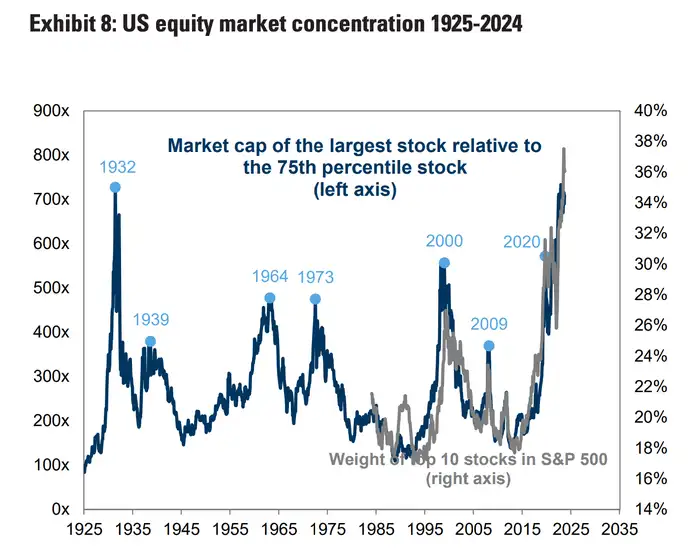

Second, market concentration is near its highest level in 100 years, Goldman said.

“When equity market concentration is high, performance of the aggregate index is strongly dictated by the prospects of a few stocks,” the analysts wrote.

These stocks include tech large-caps such as Nvidia and Alphabet, whose performance has driven the S&P 500 more than 20% higher year-to-date. While that’s led the index through a string of record highs this year, it fosters a market mired in volatility risk and in need of diversity.

“Our historical analyses show that it is extremely difficult for any firm to maintain high levels of sales growth and profit margins over sustained periods of time. The same issue plagues a highly concentrated index,” Goldman said.

While some may find reason to argue why tech stocks will maintain growth momentum, history suggests that revenue will slow. According to Goldman, S&P 500 firms that have consistently generated over 20% revenue growth underwent a sharp drop off after 10 years.

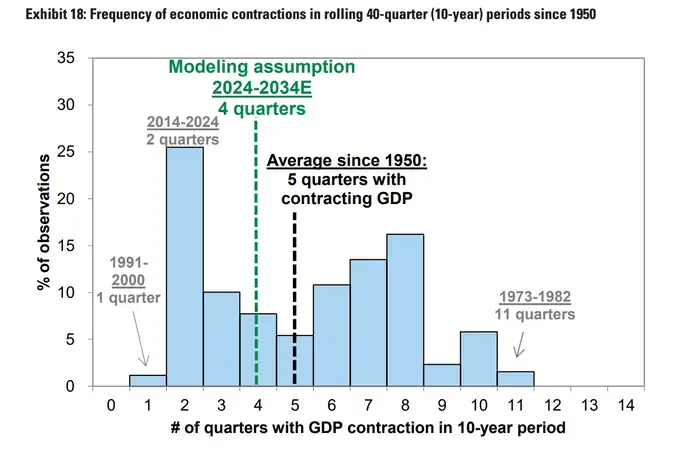

Third, Goldman expects the economy to contract more frequently for the next decade. The firm says the US will see four GDP contractions over the period, or in 10% of quarters. That’s up from two such instances during the previous decade.

Goldman notes that annualized equity returns typically average -10% during these periods of economic slowdown.

The fourth headwind factored into Goldman’s forward-return model is corporate profitability. The firm tied its rationale in with the concentration argument above, saying that as sales and earnings growth decelerate for the market’s biggest stocks, that will have an outsize impact on the entire market.

Finally, the fifth is the relative level of the 10-year Treasury yield. The 10-year is currently yielding north of 4% as investors recalibrate their rate-cut expectations following a series of strong economic-data reports and amid persistently hot inflation.