Investing legend Rob Arnott says it’s an ‘extraordinary opportunity’ to make these 3 trades set to deliver over 10% annual returns for a decade — crushing large-cap stocks

Clerks and traders in the Euro Dollar pit at the Chicago Mercantile Exchange celebrate the New Year at the close of trading on the last business day of the year December 29, 2006.

Research Affiliates Founder Rob Arnott sees a bear market ahead for large-cap growth stocks. That spells trouble for the S&P 500, which is heavily made up of giant growth stocks like Apple, Microsoft, and Nvidia.

But just because prospects for the index look poor doesn’t mean other pockets of the market won’t do well, Arnott told B-17 earlier this month.

While he expects the S&P 500 to return 3% annually, on average, over the next decade, Arnott said a few other trades are in much better positions to outperform, given their low valuations.

Small-cap stocks, small-cap value stocks, and non-US value stocks are all poised to deliver at least 10% returns annually over the next 10 years, he said.

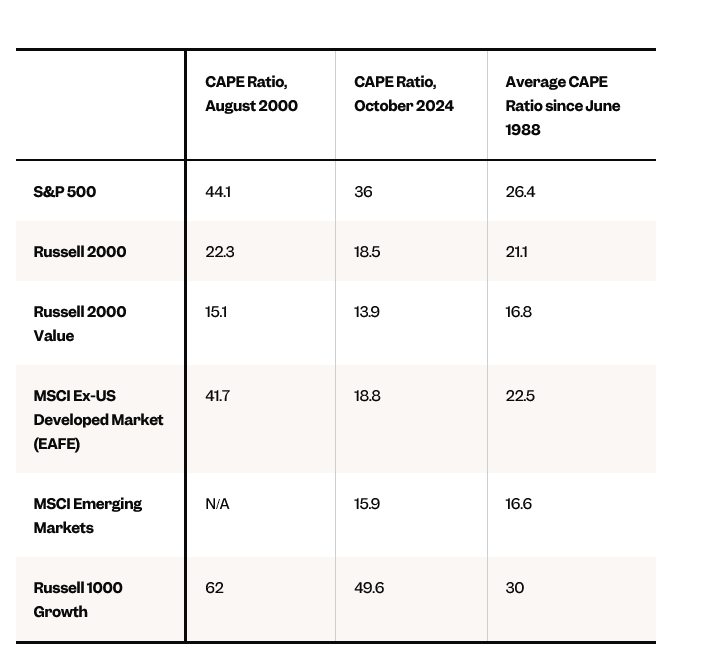

Arnott’s estimates are simply the product of valuation levels and historical returns associated with current levels. While the S&P 500’s CAPE — short for cyclically adjusted price-to-earnings — ratio is 38, indexes tracking these other parts of the market are valued at much lower levels.

US small-cap stocks, measured by the Russell 2000 index, trade at about a 19 CAPE ratio. The gap between value and growth stock valuations is about as wide as it was during the dot-com bubble in 2000, Arnott said, with the Russell 1000 Growth index sitting at around a 50 CAPE ratio.

Small-cap value stocks (Russell 2000 Value index) are also cheap, with a 14 CAPE ratio.

In non-US value, emerging markets, Japan, and Europe all look historically cheap, he said. Japan and Europe’s CAPE ratio sits around 19. The CAPE ratio for emerging market stocks, meanwhile, is about 15.

“That’s a hell of a big spread,” he said. “So I look on all of this as an extraordinary opportunity.”

Again, in addition to delivering robust returns in the long term, Arnott believes these areas of the market could very well surge even if tech stocks implode, which would presumably bring down indexes like the S&P 500. That’s exactly what happened at the start of the dot-com bubble, he said.

“It’s fascinating to note that, from March 2000 to March 2002, the S&P was down 27%, while Russell 2000 Value was up 53% (Russell 1000 Value and the full Russell 2000 were both flat, shrugging off a nasty bear market); then everything fell about 25% through end-September,” Arnott wrote in a follow-up email.

“When valuation gaps get wide enough, markets can utterly disconnect,” he continued. “Could the Mag-7 bubble burst, while small-cap, value, and small-cap value all shrug off the carnage? Sure, it’s happened before.”

Investors can gain exposure to these trades through various exchange-traded, like the Avantis U.S Small Cap Equity ETF (AVSC), the Vanguard Russell 2000 Value Index (VTWV), the iShares MSCI EAFE Value ETF (EFV), and the Dimensional Emerging Markets Value ETF (DFEV).