5 charts show stock market valuations are stretched to historical extremes

The stock market has been on a tear this year, with the S&P 500 surging 27% and minting more than 50 record closing highs.

Interest rate cuts by the Federal Reserve, strong corporate earnings, and a Trump election win have all helped push stock prices to new records.

With those massive gains have come soaring valuations, and they’re starting to hit historical extremes, according to Yardeni Research.

“We wouldn’t like to see them go any higher because that would force us to raise the odds of a 1990s meltup scenario from our current subjective probability of 25%,” Yardeni Research said in a Tuesday note.

While the research firm has a bullish outlook on the stock market, predicting that a Roaring 20’s-style rally could be at hand over the next few years, it’s also cautious of current valuations.

These five charts show how stretched market valuations are.

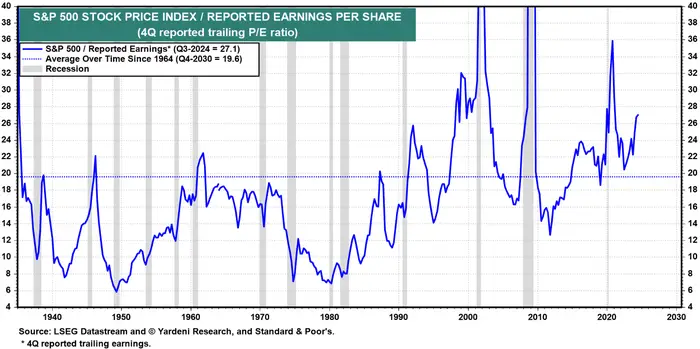

1.Trailing price-to-earnings ratio

The trailing 12-month price-to-earnings ratio surged to 27.1x in the third quarter. While not near its highest level ever, it’s well above its long-term average of 19.6x.

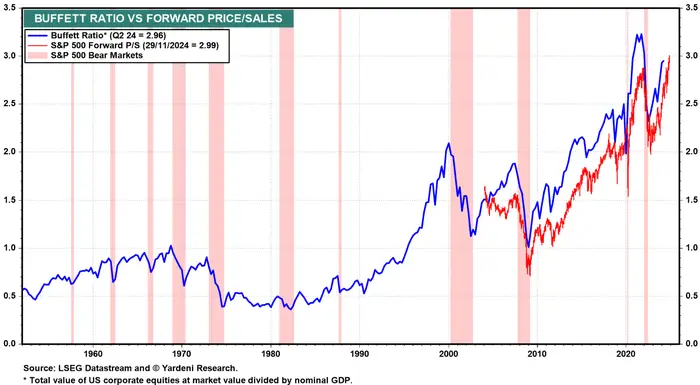

2.The Buffett ratio

This valuation measure, popularized by Warren Buffett over two decades ago, measures the total value of US stocks relative to nominal GDP.

The valuation measure rose to a record high of 2.96x in the second quarter. Buffett has previously said that when the ratio rises above 2.0x, it suggests the stock market is overvalued.

“That might explain why he has been raising so much cash in the portfolio he manages for Berkshire Hathaway,” Yardeni Research said.

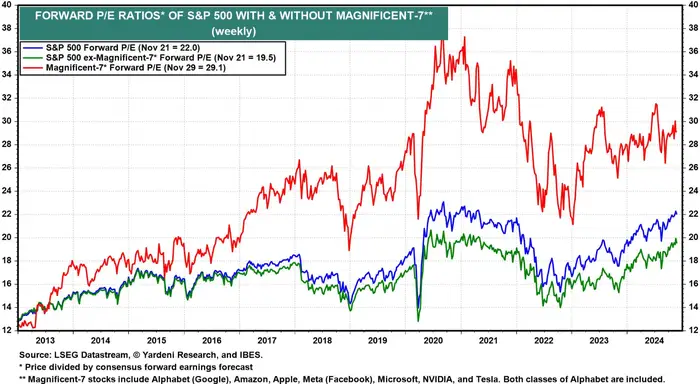

3.Forward price-to-earnings

The forward price-to-earnings ratio, which is based on forward-looking analyst estimates for corporate earnings, is nearing the peak seen during the stimulus-driven stock market rally of 2020 and 2021.

At 22.0x, the forward P/E ratio is within spitting distance of the 25.0x record high reached during the dot-com bubble in 1999.

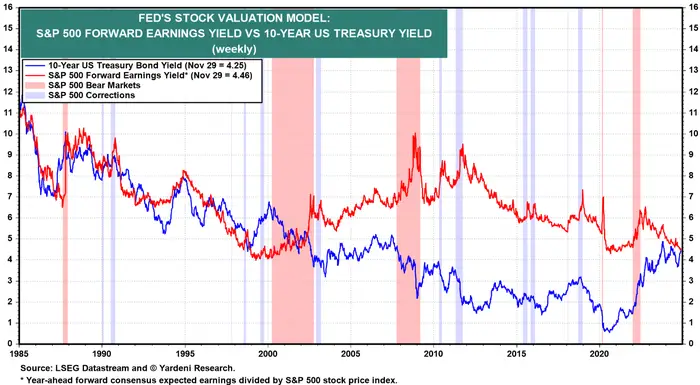

4.The Fed model

The Federal Reserve has a stock market valuation model that compares the forward earnings yield of the S&P 500 with the 10-year Treasury yield.

When the two yields converge, it can suggest the stock market does not have an attractive valuation.

“The model may be worth monitoring again now that the forward earnings yield at 4.46% is almost identical to the 10-year Treasury bond yield,” Yardeni Research said.

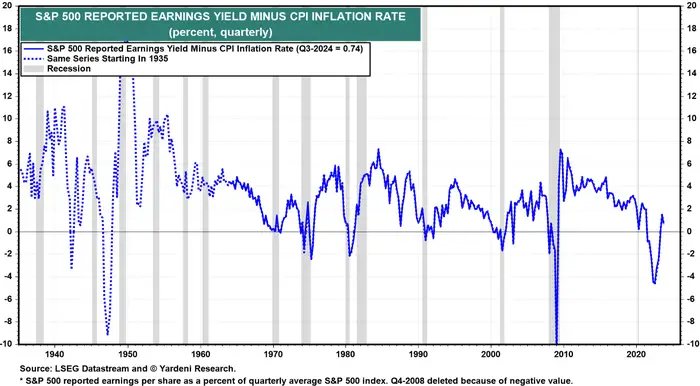

5.Real earnings yield

The spread between the S&P 500’s earnings yield and the CPI inflation rate is another valuation measure to monitor.

Yardeni Research highlighted that the valuation measure tends to be negative during economic recessions and bear markets.

With the valuation measure being only slightly positive for the past six quarters and trending lower, it’s another valuation measure to keep an eye on.

Ultimately, valuation measures have proven to be poor market timing tools. There’s nothing stopping the stock market from getting even more expensive before its next bear market correction.

“Investors will pay a higher P/E the longer they believe that the economic expansion will last. That’s because time is money. The longer the expansion, the longer that earnings have to grow to justify the current multiple,” Yardeni Research said.