The Trump trade: how a red wave could impact stocks, bonds, and commodities

As we near the November elections, investors are increasingly focused on what a Donald Trump win would mean for global markets and economies.

Prediction markets assign a 70% probability of a Trump victory, according to a July 17 note from Goldman Sachs. The failed assassination attempt on the former president rallied further support for him. Bets on election results spiked 116% that day on Predictit, heavily favoring his win.

Political speculators weren’t the only ones throwing money at their expectations. Investors and traders alike took their outlooks to the stock market. A more obvious play sent shares of Trump Media and Technology Group (DJT) up by 31% on Monday. That day, the broader market rallied, too.

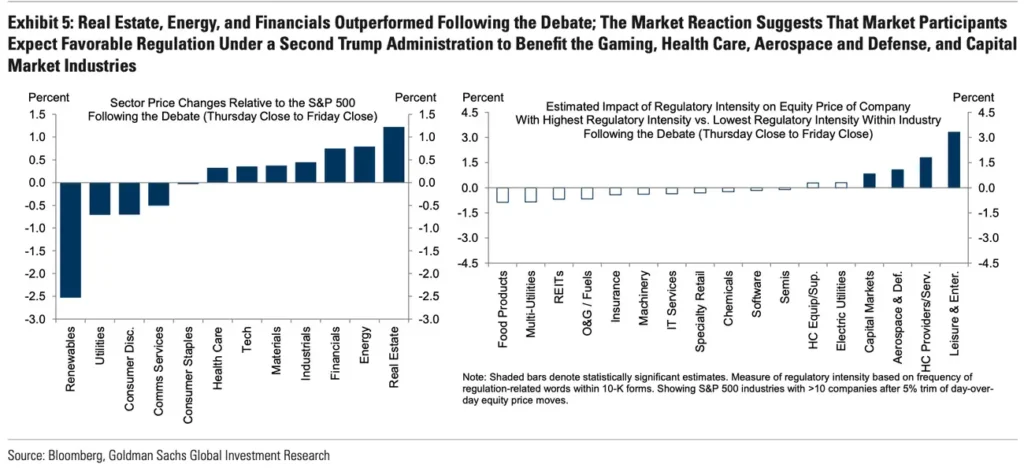

The presidential debate, which proved disastrous for President Joe Biden, showed some sector-specific bets investors made in anticipation of a Trump win. Investors opted for real estate, traditional energy, financials, and industrials while dumping renewables and utilities stocks. The charts below show how stock sectors moved in the 24 hours after the debate and how a Trump administration might impact sectors with varying regulatory burdens.

Despite the market’s expectations, a team at UBS led by Americas Global Wealth Management CIO Solita Marcelli warns investors about being hasty and making premature adjustments to their portfolios based on skewed subjective reactions.

Samantha Lamas, a behavioral researcher at Morningstar, told B-17 that investors are highly exposed to behavioral blunders because their confirmation biases will tilt them toward accepting information that aligns with their beliefs. She also warned against the scarcity mindset accompanying a deadline: in this case, the upcoming elections could prompt investors to think they must rapidly adjust their portfolios.

If Trump wins, investors will need to cut through the noise and at least understand how he might impact different parts of the economy. That said, for Trump to navigate policy shifts more easily, he needs a red wave — Republicans winning majorities in both chambers of Congress — to increase the chances that his agenda passes without friction.

In terms of areas ripe for direct contact, Goldman lists tariffs, taxes, and regulation as central.

Policy

A deregulation agenda is top of mind under Trump’s leadership. Goldman’s Jan Hatzius and his team reviewed his previous administration’s policies in anticipation of what to expect during a second term. They found a reduction of rules for vehicle fuel efficiency standards, environmental permits, financial regulations, and internet providers.

Meanwhile, the administration increased restrictions on immigration, drug prices, and nicotine products. The investment bank expects that a second Trump term will look the same but with more rollbacks on energy and environmental policies, which could be negative for renewables and positive for more traditional forms of energy. They also expect a loosening of financial regulations, which could be good for banks.

Where monetary policy is concerned, leading economist Christophe Barraud believes a Trump administration could pressure the Federal Reserve to be very accommodative on rates, in other words, steeper or sooner cuts. But in a recent interview with Bloomberg Businessweek Trump advised against lowering interest rates before elections, citing concerns of inflation.

Either way, UBS highlighted that it wouldn’t be the central bank’s first encounter with increased criticism from an elected official. It expects the Fed will maintain its independence, adding that political interference would be perceived as counterproductive by markets anyway.

Tariffs

A note from Goldman’s European portfolio strategists maintains a scenario in which a blanket 10% tariff on all US imports could apply, regardless of where those goods are coming from. This would hit the global economy and US consumers, who’d pay higher prices for their imported purchases.

In 2023, the US imported more than $3.8 trillion in goods, making it the world’s largest importer.

Mexico, Canada, and China are its biggest trade partners. But according to Goldman’s report, China, Japan, and Germany are likely to see the most impact because manufacturing makes up a large percent of their GDP.

European industries most exposed to US tariffs are those with the highest percentage of goods sold to the US, according to Goldman’s strategists. At the top of the list is machinery and equipment, where 29% of the products end up in the US, followed by pharmaceuticals at 19%, and chemicals at 12%. In European equities, Goldman’s team recommends taking a long position on the names that own US-based assets and businesses while avoiding European autos and chemicals.

On a global scale, the last round of trade wars under Trump’s administration hit stocks from emerging economies the hardest. The chart below, from Goldman Sachs, demonstrates that China’s Hang Seng Index (HSI) saw the steepest drop in returns when tariffs were announced, followed by the Korea Composite Stock Price Index (KOSPI), and then Asia Pacific’s MSCI Asia xJP Index

US markets

Making an expectations-based bet on US equities could be tricky, and even the biggest banks don’t agree on the best plays. In general, Goldman noted that sectors with the highest exposure to political uncertainty, whether positively or negatively, include energy, utilities, financials, healthcare, industrials, materials, and telecommunications. Meanwhile, those with less exposure are consumer discretionary, staples, technology, and real estate.

But UBS warns that a Trump presidency and a Republican Congress could create headwinds for US consumer discretionaries if higher tariffs become effective.

UBS also puts renewables in the danger zone because the sector will likely see less government support. This parallels Goldman’s review of Trump’s past policies, which cut back on budgets and permits for environmental protections and energy, and its expectation of further rollbacks under another term.

A Republican sweep could also bring about tax-cut extensions, according to a June 14 note from Morgan Stanely. This would benefit industrials, telecommunications, healthcare, and tech.

If all this sounds messy, and you don’t want to take sides, Morgan Stanley highlights a win-win bet: the defense sector is expected to benefit regardless of who takes office because both parties are motivated to spend on national security.

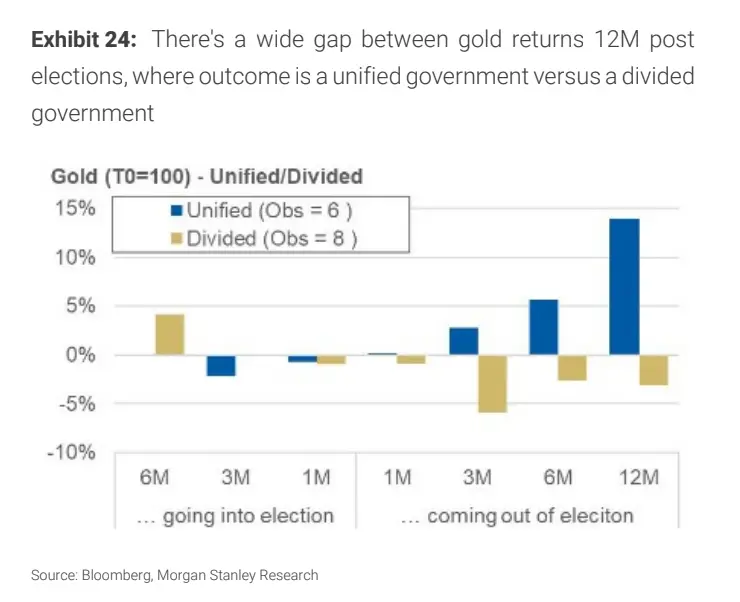

In commodities, UBS likes gold since investors may see it as a hedge against geopolitical risk, inflation, and government deficits. But Morgan Stanley emphasized that gold’s post-election returns lean heavily on the outcome of a unified government, which is when the president and majority of Congress are same-party members.

A chart from the investment bank below demonstrates that the commodity’s 12-month return post-elections are only positive under a unified government.

In commodities that are part of the energy play, Goldman likes liquefied natural gas (LNG). It expects a Trump Administration to allow LNG export permits after the Biden Administration attempted to halt them. The bank also believes the oil and gas industry will be favored as obstacles impacting its development will be eased through an expansion of oil leases on federal land and offshore, and a rollback of the restrictions placed on refineries and methane emissions.

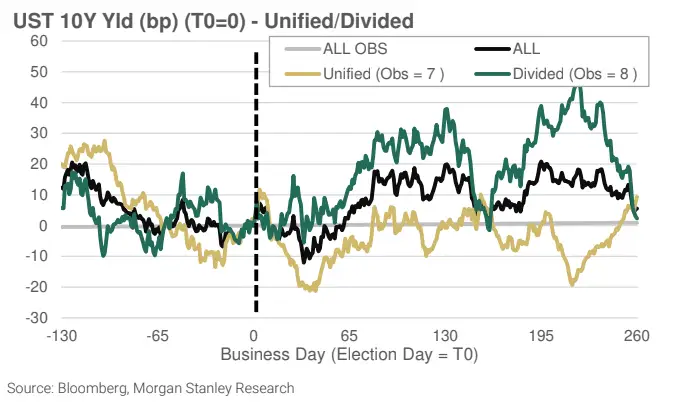

Fixed income is another area that could be impacted. While Washington may have limited influence on central bank policy, how bond-buyers respond is another story. There has been an observable correlation between elections and the 10-year Treasury: in the six months leading up to voting day, rates historically fell, but were then followed by uncertainty, according to Morgan Stanley. The investment bank forecasts a lower yield under a divided Trump government. But under a sweep, it expects mixed to slightly higher yields.

Below is a chart from Morgan Stanley demonstrating 10-year yields in the 130 days leading into elections and onwards.