A longtime bull who called this rally shares a ‘common sense’ strategy to capitalize on another strong year for US stocks

Wall Street should prepare for further gains in 2025, according to BMO Capital Markets.

Investors appear to be in for another excellent year in 2025, even though US stock returns will likely normalize after years of explosive gains.

The S&P 500 is set to rise 13.7% to 6,700 in 2025, according to BMO Capital Markets. That would align neatly with the 15% earnings growth rate that analysts are calling for, as well as the market’s average return of 14% since 2009.

While a sixth double-digit gain in seven years should be a cause for celebration, BMO’s projection would be the S&P 500’s most modest positive return since 2016. Market participants have been spoiled recently, as the index has soared 23.6% in 2024 after a 24.2% jump in 2023.

The current backdrop, which is marked by healthy economic growth and moderating inflation and interest rates, provides a promising setup for further gains, BMO strategists predicted.

But Brian Belski, BMO’s chief investment strategist, suspects this rate of gains isn’t sustainable, considering how far US stocks have risen and where valuations are.

“It is clearly time for markets to take somewhat of a breather,” Belski wrote in a new note about his firm’s 2025 market outlook. He later added: “We are approaching the upcoming year with slightly more caution compared to our market outlook from last year, given the degree of market gains and valuation expansion that has occurred over the past two years.”

Why history says to be more optimistic than cautious

Despite that warning, Belski remains one of the most bullish strategists on Wall Street.

At times, BMO has set overly ambitious price targets for the S&P 500. The Montreal-based firm thought the index would climb 11% in 2022, before slashing its target midway through that year. US stocks eventually slid 19.4% in what became the worst year for stocks since 2008.

Undeterred by those misses, Belski and his team called for a double-digit rebound for the index in each of the next two years. And although BMO was one of the most bullish investment firms both times, it still underestimated US stocks, though by much less than its peers.

That persistent optimism may create the impression that Belski is always bullish, though that’s not the case. The investment chief bristled at that charge last year, but now, he’s embracing it.

“While our work is routinely labeled as being ‘perma-bullish,’ we will gladly accept that moniker,” Belski wrote.

Unlike the permabulls or permabears who refuse to adapt to new evidence or admit defeat, Belski’s convictions are based not on confirmation bias, but historical precedent.

“We prefer a common sense, and yes more humble, approach to investing versus trying to prove that our narrative is always correct,” Belski wrote.

Betting against US stocks for an extended period of time is almost always a losing proposition. In the 15 years since the financial crisis, the market has risen close to 85% of the time and at an annual rate in the mid-teens, while losses have been comparatively mild at around 6%.

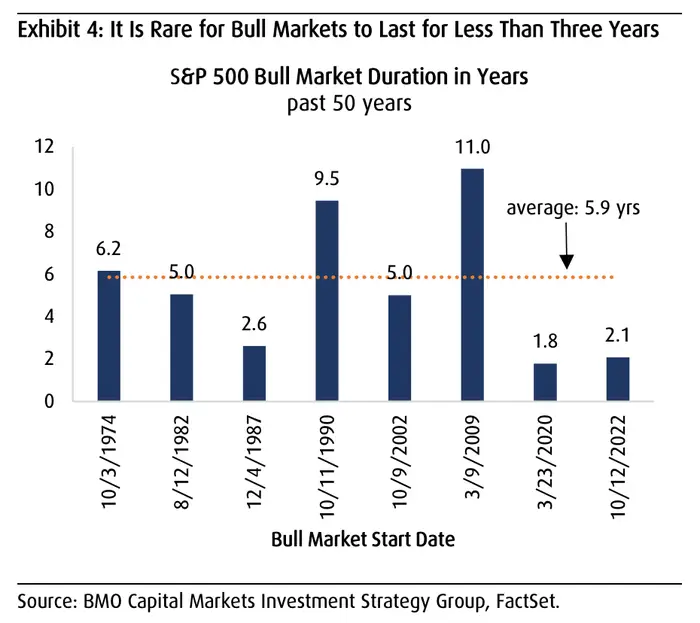

Even more astounding is that in the last five decades, the S&P 500 tends to go nearly six years without suffering a 20% pullback, which is the bar for a bear market.

To that point, bull markets — which are marked by a 20% gain from the market trough — have lasted at least five years in five of the last seven instances, and one of those misses came during the pandemic. Barring a major upset, this two-year-long bull market will extend that trend.

How to invest as returns become harder to come by

The years immediately after the pandemic have been full of twists and turns that seem obvious in hindsight, but were impossible to predict at the time.

However, Belski now thinks the market outlook looks refreshingly simple, especially since the US elections are over. Solid earnings and a healthy economy seem like a recipe for success.

“An environment of high-single-digit annual price gains coupled with at, or near, double-digit earnings growth and price-to-earnings ratios in the high teens to low 20s over the next few years would be a good start on the path to normalization,” Belski wrote.

If all goes right — as in, economic growth continues to beat expectations, inflation stays in check, and interest rates fall — the S&P 500 could reach the 7,000 milestone, in BMO’s view.

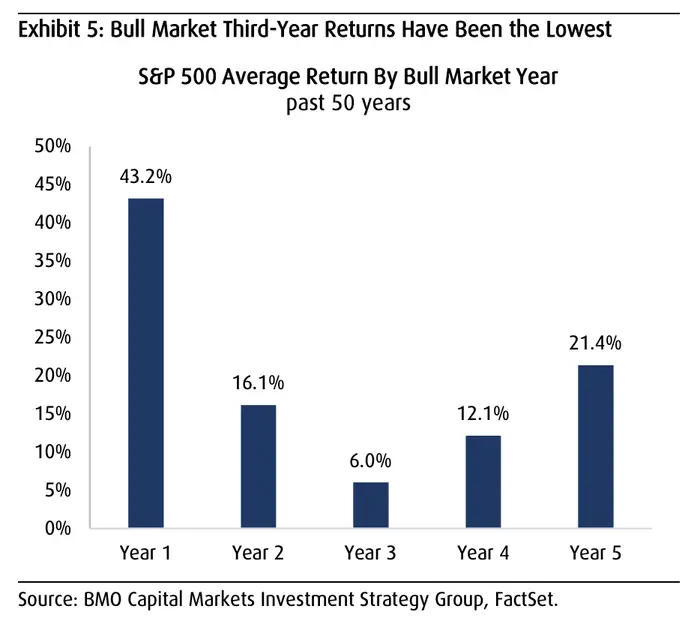

But a let-down year is also on the table, Belski warned. The third year of bull markets tends to be weaker anyway, and if inflation heats back up — along with unwanted rumors of rate hikes — the S&P 500 could retreat to the 5,500 level.

“We still see stocks continuing their upward trend for years to come, but the nearer-term path is likely to become more challenging, if history is any sort of guide,” Belski wrote.

Even still, there will be plenty of ways for investors to make money in 2025. Best of all, Belski said they don’t need to overthink their asset allocation decisions.

“Annual financial market forecasts are typically accompanied by shiny new recommendations,” Belski wrote. “However, if you do not have to, why outsmart yourself?”

In that spirit, BMO recommends building, or maintaining, a diversified portfolio made of stocks across styles and sizes. The firm doesn’t think it’s necessary to tilt toward growth or value, or even choose between large, mid-sized, and smaller stocks — despite recent market shifts.

“Investors will need to own a little bit of ‘everything’ and not tilt too far in one direction or another from a sector, style, and size perspective,” Belski wrote.

With that said, some sectors look more attractive than others. BMO is most excited about two parts of the market: technology and financials. Those are its two top picks from 12 months ago.

“Technology remains THE growth vehicle in global markets, while financials are drastically unloved,” Belski wrote. That latter point is starting to change, as financials have been one of the hottest sectors in the last month. “Less regulation and consolation are on the way,” Belski noted.

Additionally, BMO also has an overweight rating on the consumer discretionary sector, though the firm is preaching selectivity outside of Amazon and Tesla — the two titans in the cohort. That’s fitting, given that a cautiously opportunistic approach may be key to success in 2025.