A world-champion quant trader with a 491% annual return shares an easy pattern that’s profitable in 72% of test samples and can be manually executed

Ivan Scherman is a certified chartered market technician and a hedge fund manager out of Buenos Aires, Argentina.

He trades the spot, futures, and options markets across stocks, indexes, commodities, and currencies — basically, anything that can be accessed through the New York Stock Exchange, the Chicago Mercantile Exchange, and other major US exchanges.

And he’s good at what he does: in the 2023 World Cup Championship of Futures Trading, Scherman finished first with a 491.4% return, according to competition records.

Here’s the thing: while wielding such gains sounds enticing, he can’t do it as a human.

Scherman is a quant fund manager who can use hundreds of models to help execute trades. His job is to backtest models and then put them to work while monitoring their progress. The machine allows him to diversify in the true sense, trading across multiple assets, from the S&P 500 to coffee and even soybeans.

His trading journey didn’t begin as a quant expert or even a trader. In 1996, he was a law student at the University of Buenos Aires when he became intrigued with markets after taking a course in trading and securitization. His interest led him to pursue a certificate in trading at the Argentine Financial Markets Institute.

The more he learned, the more he gradually made small trades as a side hustle during his first few years as a trademark attorney.

“At the very beginning, I thought I knew how to trade, but I didn’t. It was a bull market. I was trading in the Argentina market,” Scherman said. “So whatever I traded, I made profits. When things started to get tough in the Argentina market, I broke my account.”

It was an experience that pushed him into wanting to adapt an approach that would omit human error, often resulting from emotional reactions.

Crafting his skill

It took him about four years of failing to become a decent trader, but that didn’t mean he was a good fund manager. When he left law to become a professional trader, his shortfalls were cushioned by his firm’s risk department, which prevented him from taking on big losses in his trades. But he still took on losses in his personal account because he hadn’t learned to manage risk independently.

A book he read, “Evidence-Based Technical Analysis,” by David Aronson, taught him how to apply a scientific method to design or test a trading hypothesis. One of those lessons was that a trader’s strategy should be tested in every market condition, including in bull, bear, and flat markets with high to low volatility. This is because a trader can’t predict the next market regime and must prove that their thesis can survive changes. The larger the historical sample, the better off the trader will be.

Through further trial and error, he learned additional lessons on risk management. The two major ones were that he shouldn’t put all his efforts into one trade and must treat each attempt like it could be a big loss. Instead, he should aim for small gains across different positions and include a stop loss based on historical data for each thesis.

In his backtests, he looks for repetitive behaviors to identify stop-loss points and measures their range to determine how they failed and the depth of losses they historically produced. The stop loss will be set differently for each thesis. For example, if a certain pattern often drops by 2% before becoming a winner, he will set a wider range early on so the trade doesn’t get stopped out. The outcome is that the stop loss will vary for each pattern based on its historical behavior.

Finally, he limits overall risk by keeping each position small, between 2% to 3% of his full portfolio.

“I need to have the capital to recover from that loss,” Scherman said. “There are certain numbers that I have in my mind that are very important to me. For example, if you lose 10%, you’re going to need 11% to recover that loss. If you lose 20%, you’re going to need around 33% to recover from that loss. If you lose 50%, you will need to make 100% to recover that loss.”

While he uses models to backtest his theories, a trader could replicate this process by reviewing trading charts for every asset and pattern they trade to determine the ranges a pattern can pull back with. Still, each stop loss should be tailored to a trader’s personal risk tolerance and capacity.

A simple trade from a quant manager’s tool book

While much of what Scherman does can’t be replicated by a human, some tips and patterns can be drawn from his models.

Mainly, a trader must learn to take a technical approach that’s evidence-based and built on historical patterns rather than subjective opinions. In algorithmic trading, there is no interpretation of the behavior of patterns. Instead, every rule, such as what an uptrend is, will be quantified and understood by the computer. So, what can be understood by a compute, can be understood by a human, he noted.

As for a strategy out of his models’ playbook, while it’s not a pattern he uses, a simple one that a human can replicate is to trade the S&P 500 using moving-day averages.

Here, two conditions must be met:

First, the 200-day moving average of the day is greater than the previous day.

Second, the S&P 500 has three consecutive days of lower closes than each previous day. This decline, following the first trend above, indicates that there’s a temporary pullback on a strong uptrend.

Scherman noted that considering the market moves in swings, it will close above the five-day moving average at some point.

“When it closes above the five-day moving average, it produces profits in 72% of the samples tested for 100 years.”

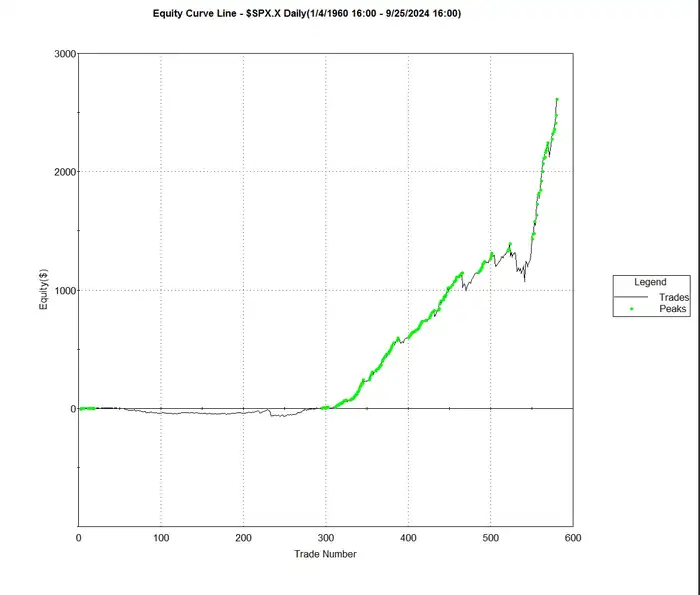

The chart below shows gains that could hypothetically be accumulated over the number of trades where this pattern occurred since 1960 based on buying one unit of the SPX, according to proprietary trading models tested by Emerge Funds Investments until September 2024.

Scherman noted that the closest way to replicate the index’s output is with a major ETF that tracks it, like the SPDR S&P 500 ETF (SPY). While there might be slight variations due to frictions including execution-price differences in an actual trade, the winning rate will remain the same.

The chart below shows how the pattern may appear on a chart and the hypothetical entry and exit points. In option one, the trade is automatically taken before the market closes on the third day of the lower consecutive close and sold on the close of the day it’s above the five-day moving average. Option two in the chart is a second way to enter the trade by buying at the next open after the third consecutive lower close and exiting at the next open the day after it closes above the five-moving average.

However, the model shows that option one has better performance outcomes.