Baby boomers have a ton of their wealth tied up in stocks and housing. Here’s why that’s a risk to the economy.

One of the economy’s most powerful engines may be at risk.

That’s because baby boomers, America’s second-largest and richest generation, could abruptly dial back their spending at the first sign of economic or market turmoil, according to Brij Khurana, a fixed income portfolio manager at Wellington Management.

Khurana thinks what has made boomers the wealthiest generation — stocks and housing — also makes them a risk to economic stability.

Even a mild correction to asset prices could spook older Americans enough to rein in their spending and kick out a key support from under the economy, he told B-17.

Such a scenario is an ‘”underappreciated risk,” he said, given how much boomers’ spending habits have fueled economic growth in recent years.

The generation is already flashing early signs that their spending power is starting to wane. Despite shelling out on travel in recent years, just 19% of baby boomers said they planned to splurge in 2024, according to a McKinsey & Company survey, lower than the average 38% recorded across all generations.

Boomers are also signaling that they’re beginning to rotate out of stocks and into longer-duration fixed income, Khurana says, pointing to the rally in long-dated US Treasuries. The iShares 7-10 year Treasury bond ETF is up 6% over the last year.

“I do think that’s partly due to some asset allocation shifts that have been taking place,” Khurana said.

The shift to bonds from stocks is a normal occurrence as people get older and move to protect their wealth after years of accumulation. However, other commentators have noted that as boomers reposition en masse, they risk shocking the market and prompting bouts of volatility as they sell down their stock holdings.

Also, given that they don’t have as long of a time horizon as younger investors, boomers may be prone to panic selling in a downturn, exacerbating market losses as they look to minimize their own downside.

Khurana said he pegs the odds of a recession in the next two to three years as higher than 50%. That’s in line with the outlook from New York Fed economists, with central bankers pricing in a 61% chance the economy could tip into recession within the next 12 months, per their latest projection.

“If asset prices, even if they fall from very high levels — even if they fall, call it 10% — then I think that psychologically really matters,” he said. “And you can see them cut back on their spending and [if] the savings rate rises, which would push the economy into recession in that world.”

The biggest spenders

What’s bad news for boomers is bad news for the economy, given how much economic growth has relied on their spending down their nest egg in recent years.

The demographic spends around $548 billion a year, more than any other generation, according to a report from marketing research firm Epsilon. Meanwhile, they tucked away the least savings among any generation last year, with the average boomer putting away just $4,059 in 2023, according to a report from the insurance firm New York Life.

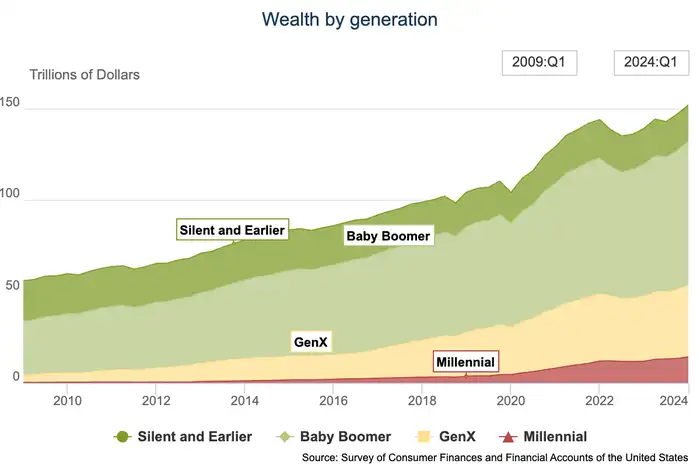

Their spending is fueled by the tremendous amount of wealth the generation is holding on to, Khurana says. Boomers were sitting on $78.5 trillion in the first quarter of this year, or the equivalent of 52% of the entire net worth of the US, according to Federal Reserve data.

Baby boomers held on to the majority of all wealth in the US last quarter.

The generation has become exceedingly wealthy because it’s holding onto the largest share of all real estate and stocks in the country, which have ballooned in value over the last five years.

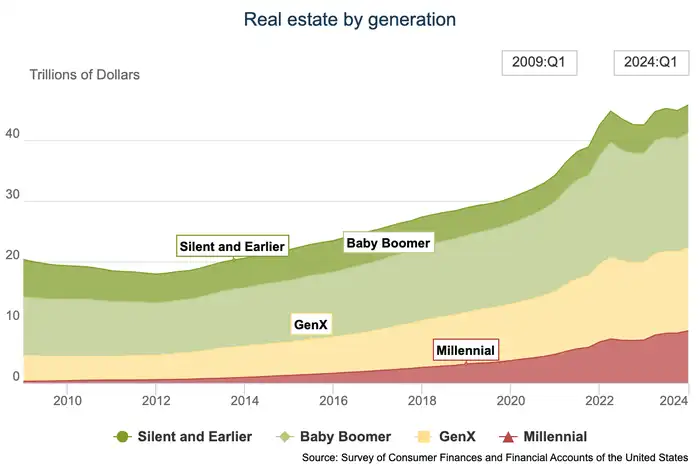

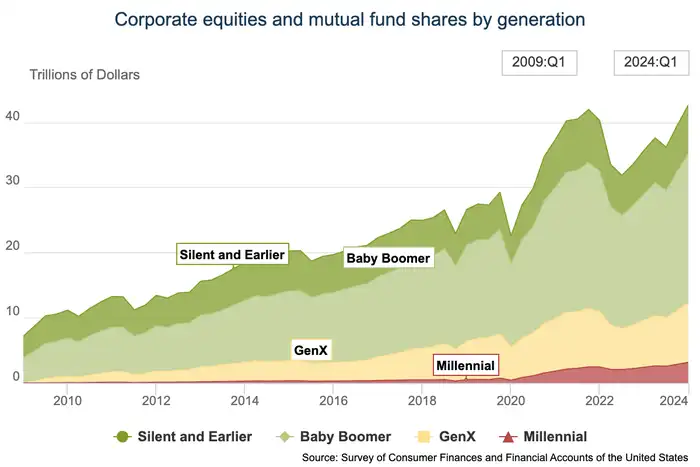

Broken down by each generation’s holdings of property and stocks, boomers accounted for 42% of all real estate ownership and 54% of all corporate equity and mutual fund ownership.

Boomers had around $19 trillion in real estate in the first quarter.

Boomers also had the largest share of corporate stocks and mutual funds, valued at around $23 trillion in the first quarter.

“What I think is happening is that, because asset prices are up, they feel very comfortable spending very aggressively,” Khurana said. “There’s no question that I think they have certainly fared better in this environment than other generations have.”

Yet, the gains they’ve enjoyed in the stock and housing market have also put boomers in a precarious position, with the group most at risk of wealth destruction if home or stock prices were to drop.

Housing and equity prices marched to record highs in the years since the pandemic, but commentators, including Khurana, think a correction in both markets could be imminent.

John Hussman, one of the market’s most bearish forecasters, estimated that stocks could have as much as 70% downside. According to one indicator tracked by his firm, the market looks to be the most overvalued since 1929, he said in a recent note.

Home prices, meanwhile, are already starting to drop in key metros that boomed during the pandemic, like cities in Florida and Texas. Home price cuts jumped to their highest level in over 5 years in August, according to a Realtor.com report.

That’s not to say boomers will cause the next recession, but the risk during a recession is dialed up under the current paradigm, Khurana said.

“I think it’s an increase in the savings rate caused by a decline in asset prices is a risk that is not on people’s radar and is definitely something that could cause the recession. And I think the probability of that is certainly higher than many people think in the next five years, or two to three years, to be honest.”