Goldman Sachs Asset Management is fired up about the economy heading into 2025 — but serious risks are still lurking under the surface

This year’s massive market rally has picked up steam in recent weeks.

Although the year ahead looks promising, top minds at Goldman Sachs Asset Management (GSAM) believe investors should be on guard for risks that could shake up the status quo.

Next year’s economic landscape may feel like an extension of this year’s, say strategists at the firm, which manages $3.1 trillion in assets. The US and other large economies are expected to pull off so-called soft landings that are marked by solid growth and easier financial conditions.

“We remain cautiously optimistic that major economies can achieve a new equilibrium of sustained growth as central banks gradually ease policy,” GSAM strategists wrote in a note about their 2025 outlook.

But that positivity shouldn’t be confused with overconfidence, as strategists added immediately after that “tail risks could knock things off balance.” GSAM investment co-chief Alexandra Wilson-Elizondo outlined potential headaches, and listed opportunities, in a recent interview.

Inflation, tariffs could cause trouble in 2025

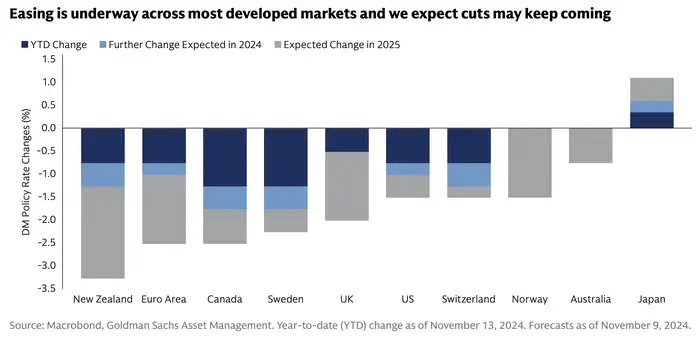

Lower interest rates are at the heart of GSAM’s upbeat thesis. The market is pricing in two to four interest rate reductions by next December, including one or two cuts by May, which would juice economic activity by reducing borrowing costs for individuals and businesses.

However, the market has dialed down its rate-cut forecast in the last month, following President-elect Trump’s victory. While Wall Street is excited about the incoming administration, some are worried that new tariffs will give inflation a second wind, thereby postponing rate cuts.

“A second Trump presidency involves upside inflation risks due to the prospect of tariffs, raising the prospect of a Fed pause and a slower pace of cuts,” GSAM strategists wrote in their note.

The market might greatly enjoy an encore of Trump’s first term, which was focused on tax cuts and deregulation. But another wave of tariffs — which are designed to boost American industry but could cause trade wars that hurt growth and drive prices higher — may be less welcome.

“We think that there’s an additional delta between what we’ll refer to as Trump 1.0 and Trump 2.0, in terms of the timing and the release and then the ultimate sequencing of things,” Wilson-Elizondo said on a webinar about GSAM’s 2025 outlook. “And that is going to give the market a little bit of digestion issues, we think, in the first quarter.”

Still, Wilson-Elizondo remarked that although investors crave rate cuts, the global economic expansion has marched on fine without them.

“The market and the economy have adjusted to [the fact that] we’re in a higher-rate world,” Wilson-Elizondo told B-17. “In terms of what the market needs, I would say that the cuts that are priced in are important from a psychological perspective. But what you can see is, a lot of the things that drive the economy, which are investment and consumption, are really quite robust.”

Like the economy, corporations can also be resilient, especially since they should have plenty of time to react to changes in trade policy. Analysts see S&P 500 profits rising about 14% in 2025, due to catalysts like deregulation and fading wage growth.

“We’re expecting that to have some impact on inflation,” Wilson-Elizondo said of tougher tariffs. “But it’s all a give and take here, because we’re also going to be seeing a lot of efficiencies come into the labor market, potentially.”

What may be troubling is that what corporations call “efficiencies,” everyone else calls layoffs. Companies that got burned during the widespread labor shortages of the pandemic have been reluctant to let workers go, but Wilson-Elizondo suspects that may be starting to change.

“The downside risk is that the philosophy or psychology of corporates — who had been pretty steadfast in hoarding labor because it was so hard to find — all of a sudden switches, and they find some level of efficiency, or they want to start playing more defense than offense as it relates to cost and expenses,” Wilson-Elizondo said.

That concern may be well founded, given that job cuts have been trending higher for months. The US unemployment rate ticked up to 4.1% earlier this fall, but it’s held steady since. GSAM strategists aren’t sweating about the labor market yet, but they’re watching those trends closely.

Stocks are expensive, but investable

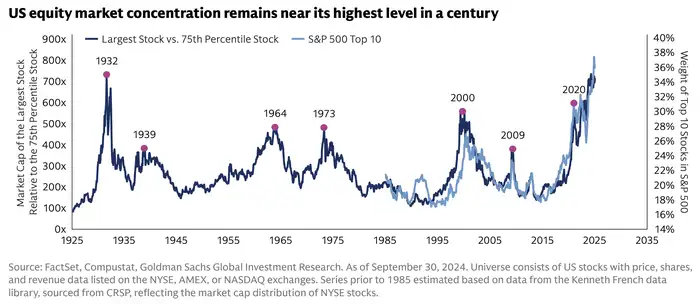

Perhaps the biggest reason for investors to worry is that their peers aren’t.

Complacency abounds, as US stock valuations are historically high by many measures, from forward price-to-earnings (P/E), cyclically adjusted P/E, and market capitalization to GDP.

One less heralded indicator Wilson-Elizondo tracks is the market’s equity risk premium (ERP), which shows how attractive stocks are relative to a risk-free return from US Treasuries. A startlingly low ERP implies that equities are an iffy risk-reward proposition at present levels.

“Ultimately, the thing we’re most concerned about is the margin of safety,” Wilson-Elizondo said. She added: “It doesn’t necessarily mean that you’re going to have a problem, but the margin for safety is really small.”

Even if concerns about trade policy and the labor market don’t materialize next year, stocks may have pulled forward gains, considering that the S&P 500 is up over 24% in consecutive years.

“When you think about the geopolitical disruption, the fact that we’re coming in at high valuations, the bar to outperform — which we saw in some single-name equities throughout earnings season — is pretty high,” Wilson-Elizondo said.

Despite their lofty valuations, GSAM isn’t bailing on US equities. Wilson-Elizondo said she sees opportunities in stocks of all sizes, including large caps other than the mega-cap growth leaders.

“We actually see — outside of the Magnificent Seven — a lot of opportunity for M&A in some of the tech space,” Wilson-Elizondo said. “And in terms of the belly of the index, which is mid caps, we see a lot of opportunity because of beneficiaries of all the themes we talked about: a stronger consumer, deregulation.”

Even so, GSAM recommends adding exposure to equities in emerging markets, which have cheap valuations and can surge on the back of lower interest rates and solid profit growth.

This often-forgotten group has been hyped as a breakout candidate for years, but has yet to deliver after posting modest mid-single-digit gains in the last two years. That may finally change in 2025 as China’s government gets serious about economic stimulus, Wilson-Elizondo said.

“Emerging markets, as a whole, have not given the return profile that one would expect over a long period of time,” Wilson-Elizondo said. “And that’s why we view emerging markets as a way to invest more dynamically.”