Millennials are making a massive financial mistakeThe generation’s obsession with cash is going to hurt them in the long run.

Cash, the ultimate safety asset in the world of investing, is suddenly the hottest trade on Wall Street.

Even with the S&P 500 up by 22% this year, Americans have poured more than $230 billion into money markets: funds holding cash and short-term debt. Typically, cash is reserved for investors who want protection in times of turbulence — the proverbial stashing of money under the mattress. But 2024 has been the second-biggest year for saving money since the 1970s, behind only 2023.

What’s notable about this flight to cash is that it’s not the baby boomers hoarding dollars for retirement; it’s millennials adding to their reserves.

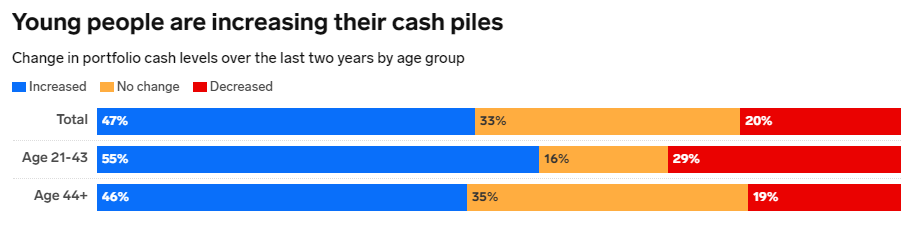

In a June survey by Bank of America’s wealth-management arm on how wealthy Americans were approaching their finances, the bank’s analysts found that over the past two years, 55% of investors between 21 and 43 had increased their cash holdings, compared with 46% of investors 44 and older. That wasn’t just young people who got worried about the economy or the risks of a sudden sell-off: The survey also suggested that younger respondents had rosy views of the economy and their finances.

I saw the same puzzling trend in investor surveys during my time at eToro, a well-known retail brokerage firm. At the end of 2023, 63% of investors 44 and younger told us they had increased their cash allocations in the past six months (versus just 27% of investors 45 or older). This, despite the fact that younger investors were more optimistic about the economy, their incomes, their living situations, and their investments.

There’s something driving younger Americans to save their cash, and I don’t think it’s solely the 5% savings rates.

Millennial investors have been deeply scarred by two life-changing crises in their young lives. For many millennials, the global financial crisis hit just as they were entering their working years. About a decade later, a once-in-a-generation pandemic — and two painful bear markets — delivered another blow to their psyches.

And now, in the prime of their investing years, the echo of those events has made them risk-averse in their investments. Millennials may be protecting themselves well with their ability to save. But when wealth is built on compounding returns over long periods, their distrust of the stock market could set them back in the long run.

Young investors have become synonymous with rampant speculation: They trade zero-day options, hop on the meme-stock rocket, or take extreme risks in the name of social-media clout. Sure, some investors adopted this devil-may-care attitude, and I’ll never judge somebody for doing what they want with their own money. But if you look at hard numbers from the Federal Reserve about what millennial investors actually own, you can see that this stereotype is misguided.

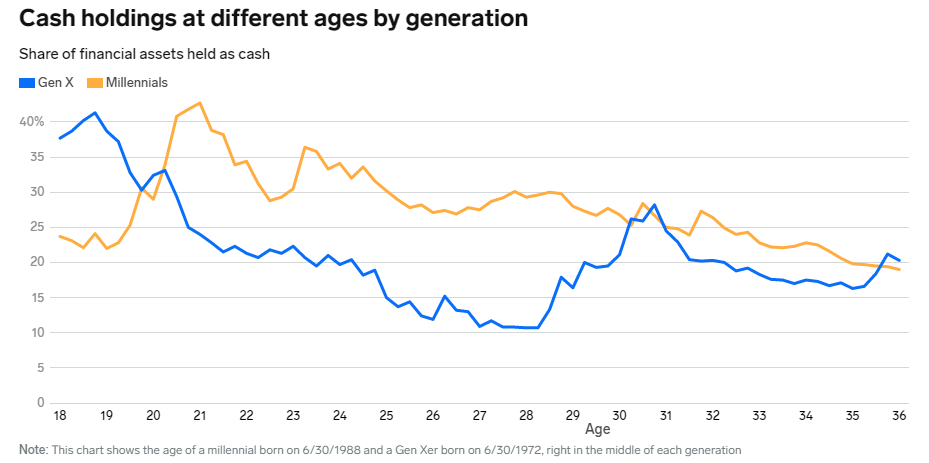

Despite their coming of age in one of the longest stock-market rallies in history, millennials had 19% of their total financial assets in cash as of June 30, the most of any generation. In a way, this makes sense — the younger you are, the less time you have to put your money toward other investments. When you compare millennials’ cash levels with Gen X’s cash levels at the same age, though, the risk aversion becomes clear. If you were born right in the middle of the millennial generation, you’re now 36. These “median millennials” held more cash as a share of their total assets during their 20s than Gen Xers did at those ages — a difference of about 13 percentage points.

What’s worse, though, is that millennials avoided stocks during some of the best years for investors. As our median millennial grew from 21 to 30, the S&P 500 grew by an average of 11.5% annually, while savings accounts paid next to nothing because of the Fed’s zero-interest-rate policy. Millennial savers didn’t just give up a precious decade of compounding — they missed one of the longest bull markets in history.

While the gap has started to close now that most millennials are in their 30s, the survey data suggests the millennial cash obsession hasn’t quite let up.

There are plenty of reasons for the recent uptick in cash allocation. Savings and money-market rates leaped as high as 5%, giving investors attractive risk-free returns; geopolitical upheaval means the world feels extremely shaky; and Wall Street pros have been warning about a recession for over a year now. But when it comes to younger investors, I think the scars run deeper than worries about a coming downturn.

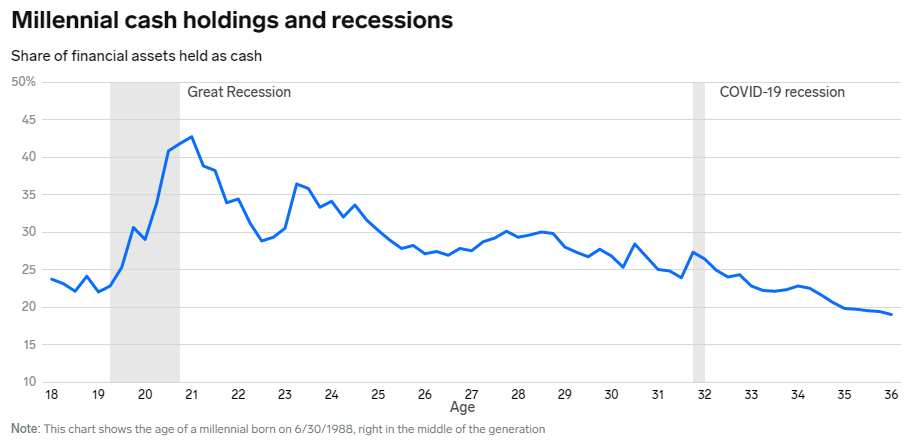

Millennials have had a tumultuous induction into adulthood. Many of them were in high school or college or in their early working years during the global financial crisis. From 2009 to 2014, the unemployment rate was 10% or higher for 20- to 24-year-old Americans. They learned to prioritize cash as they navigated one of the worst downturns in history. Then, just as they were finding their footing, the COVID-19 pandemic hit. We were locked inside our houses for weeks on end while stocks entered one of their swiftest crashes on record. Soon after, we nervously waded back into the wealth-building waters, only to get hit by scorching inflation and another bear market.

Every generation has its war stories. Gen Xers had to process 9/11 and the tech bubble bursting in their late 20s. Baby boomers dealt with their own bout of inflation and high rates as 20-year-olds in the 1980s. Their parents were unfortunate enough to experience the Great Depression, a three-year stretch of the darkest economic days in the United States. But there’s something especially pernicious about having to navigate not one but two earth-shattering crises early in adulthood.

Money can be a highly personal subject. Our feelings of financial stability develop through experiences, not classes or textbooks. A 2017 University of Michigan study found that children as young as 5 could start developing spending and saving habits. There’s also a ton of research that suggests financial stress can lead to a litany of physical, mental, and emotional issues. Early financial trauma can profoundly shape your relationship with money. That’s why personal finance can feel so illogical at times — why some of us may be set on paper but constantly fear losing it all.

I know this well. I’m a young millennial who felt the financial crisis as a teenager. My mom was a part-time bookkeeper at a housing construction company, and my dad was a residential electrician. You could probably guess what happened when the housing market went into a tailspin. I may not have been old enough to open a brokerage account, but I picked up some perverse money habits from the financial crisis that I’m trying to unlearn — even now, as the head of research at a firm that teaches people how to build wealth. Multiply this mentality across a generation, and you have one swath who brought us crypto, Occupy Wall Street, meme stocks, and YOLO capitalism, and another batch that can’t seem to take enough risks to build a decent retirement fund. These more cautious ones piled their savings into inflation-linked I-bonds — super-safe government-issued debt that locks away your money for a year — when they hit 9% in 2022. A great decision for an emergency fund, but less savvy when the stock market is plumbing new lows.

Saving too much money seems like a good problem to have, but keeping all your money in a savings account can be a huge financial mistake when you consider the opportunity cost. Imagine you put $1,000 in a savings account in July 2023 — at the peak of the Fed’s rate hikes — earning a sweet 5% APY on your cash. By October 4, you would’ve earned about $60 on that money.

How does that compare to stock-market returns? Not great.

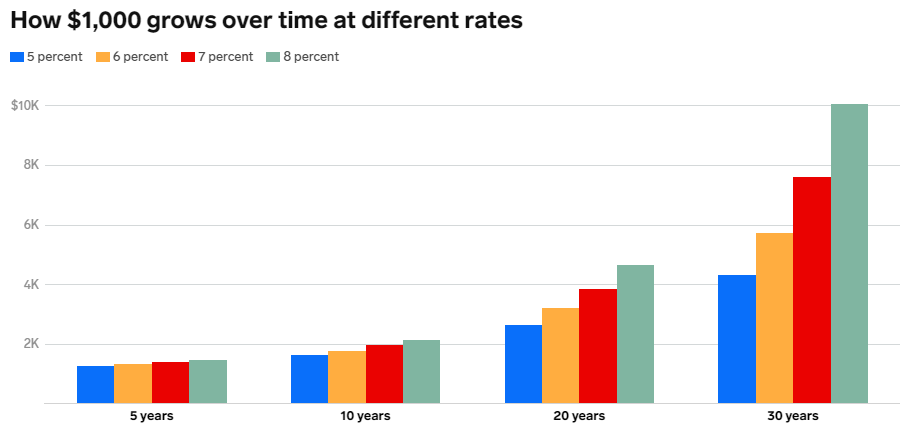

By staying in cash over the past year and change, you missed a 27% rally in the S&P 500. In other words, that $1,000 would’ve turned into about $1,277 if you’d invested it in a no-fee index fund. There were strong gains to be had in other major indexes, too: a 28% climb in the tech-heavy Nasdaq 100 and an 18% rise in the mega-company Dow. Yes, even your grandma’s index beat your cash return.

Of course, stocks and cash are different financial beasts. Cash can be dependable in tough times, and it’s often the best place to stash away funds for a big purchase. It also makes sense to have some cash on hand. Stocks, by contrast, are often far from stable. Lots of popular stocks have dropped 10% to 20% of their value in a single day, and you could theoretically lose all your invested money in the stock market. But as scary as that sounds, it’s the essence of risk-taking; you give up stability for potentially greater returns over time. If you have decades ahead of you as an investor, you’re in a prime spot to take some risks. Every little bit matters, too. Over long periods, the difference between 5% and 6% returns on a $1,000 investment can be thousands of dollars. For what it’s worth, the S&P 500 — an index of America’s largest companies — has grown by about 8% a year over the past two decades.

The long-term math favors shifting away from cash, and the short-term calculus is changing, too. Because the Fed started cutting interest rates in September, you’re slowly losing that sweet, sweet savings rate — average money-market rates have slid to 2.75% from 2.9% at the end of July.

Fellow millennials: As a market nerd who studies how the wealthiest Americans get rich, I’m begging you to stop playing it safe. Cash may feel like a warm, fuzzy blanket, but you’re not getting anything done just lying there on the couch bingeing Netflix. Holding cash as an emergency fund or a house down payment makes sense. Staking your retirement on cash doesn’t.

Risk is the foundation of wealth-building, so get off the couch.