The stock market is soaring. Wall Street’s biggest names say to be careful.

It’s been another banner year for the S&P 500 as impressive earnings and improving expectations have propelled the benchmark index to 26% returns since January.

But those increasingly rosy expectations are raising concerns among some of Wall Street’s top investors and strategists about how sustainable the rally is, and how historically high valuations may impact future returns.

A couple of widely followed valuation metrics reflect this very bullish outlook. There’s the so-called “Warren Buffett indicator,” or the ratio of total stock market capitalization-to-GDP.

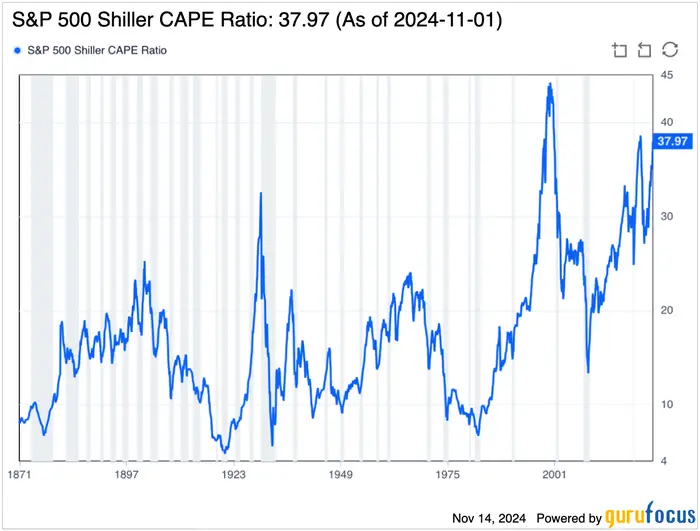

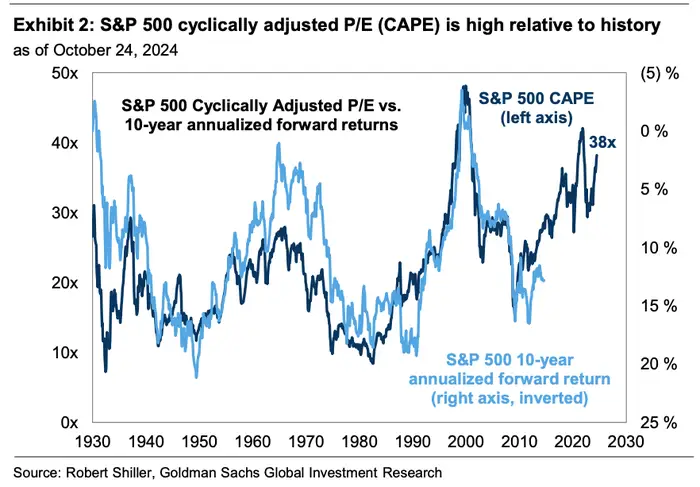

And then the Shiller cyclically adjusted price-to-earnings ratio for the S&P 500, which is a 10-year rolling average of the index’s trailing 12-month PE ratio.

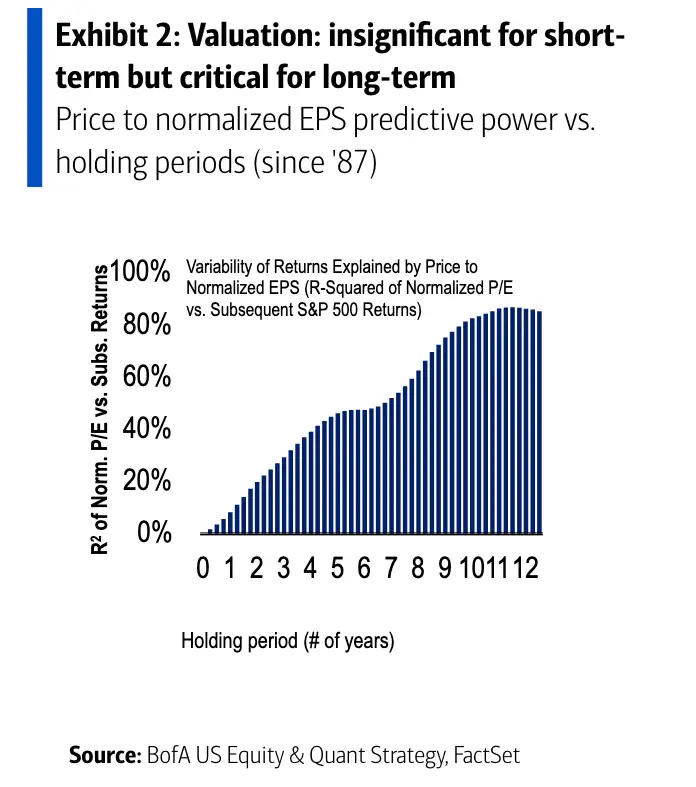

Since high valuations are an indication of lofty future expectations, they have historically meant muted returns over the long term. Expectations are either never met, or even if they are, the good performance is already priced in. Bank of America research shows that starting valuations explain 83% of the S&P 500’s returns over the following decade.

With current valuations sitting at extremes, many market experts have pointed out that returns could be relatively poor ahead. Below are comments that some of the biggest voices in market have made in recent weeks on the matter.

David Kostin, chief US equity strategist at Goldman Sachs

Kostin said in October that current Shiller CAPE ratio levels for the S&P 500 means the index is likely to return 3% on average over the next decade. For context, that’s lower than the risk-free yield on 10-year Treasurys.

Here’s that outlook shown in chart form. It illustrates well that close relationship between valuations and future market performance that Bank of America mentions.

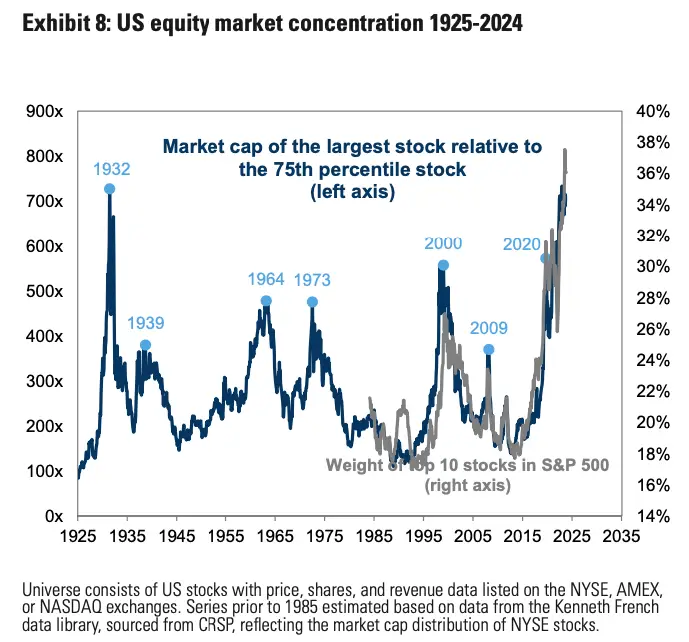

In an interview with B-17 later in October, Kostin made a couple of comparisons to the dot-com bubble, which peaked in 2000. One is that valuations for the largest stocks in the market are significantly higher than the rest of the S&P 500.

Another is that the market cap of the top stock in the index is hundreds of times larger than that of the 75th percentile stock.

“We’re at a level of concentration in the US market today that we haven’t really seen since the tech bubble,” Kostin told B-17. “It’s even more concentrated than it was 20 years ago.”

Rob Arnott, founder of Research Affiliates

Arnott, whose clients include some of the largest institutions on Wall Street, also made dot-com bubble comparisons. While he also sees poor long-term returns ahead for the S&P 500, he said that large-cap growth stocks — which make up much of the index — could suffer a pullback in the near-term.

“This looks and feels like the year 2000 to me,” Arnott told B-17 earlier this month. “Are we likely to see a bear market in the next two years for large-cap growth? Yeah.”

He said that earnings growth likely won’t live up to expectations, and disruptors in AI will take market share from current top firms.

Nelson Peltz, cofounder of Trian Partners

Peltz said at CNBC’s Delivering Alpha conference earlier in November that valuations have become too elevated, and something will come along to knock them down.

“Trees don’t grow to the sky, definitely not uninterrupted,” Peltz said, using an idiom that refers to valuations becoming disconnected from reality. “There will be something that might upset it. I think you’ve got euphoria from the election.”

Dave Sekera, chief US market strategist at Morningstar

Sekera also said on the day after the election that enthusiasm about Trump’s win and the prospect of higher growth was making the market overvalued.

“When I look at the market today, it is trading, with today’s bump, probably a 3% to 4% premium above fair value,” he said. “Now, a lot of investors may say, ‘Eh, 3% to 4% doesn’t sound like that much from a market point of view,’ but when I look at our valuations going back to 2010, less than 20% of the time have we seen the market trade at this much of a premium or more.”

He urged investors not to get caught up in the hype.

“Based on your risk tolerance, I probably wouldn’t be making any changes here today,” Sekera said. “And when you do make changes, make sure that you’re only making changes when there’s really a change in your underlying fundamentals and only make changes in your portfolio based on an informed analysis.”

Bill Smead, the founder of Smead Capital Management

Smead, whose value fund has beaten 97% of similar funds over the last 15 years, according to Morningstar data, also said that the post-election trade was exacerbating an already overvalued market.

“It’s a disaster waiting to happen,” he told B-17. “We have put the icing on the financial euphoria cake and lit the candle on top.”

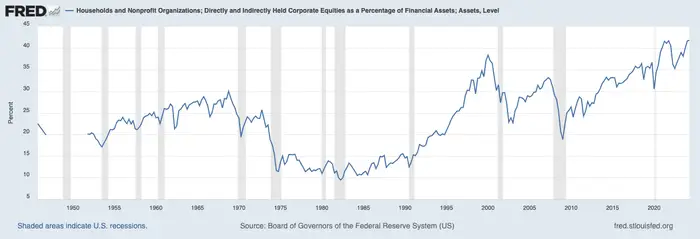

One piece of evidence showing that euphoria is the level of household equity ownership, Smead said. Right now, around 42% of household assets are in equities, the highest level in history.

Jeremy Grantham, cofounder of GMO

Grantham has been warning of a “super bubble” in stocks for a few years now, and recently reiterated his dire outlook for the market.

“Really great things happen in the internet phase, ’98-’99. But they overdo it,” Grantham said in an interview with Morningstar published October 30.”When you have these great developments, they overdo themselves in the short term, they crash in the intermediate term, and then they come out of the wreckage and change the world in the long term. And that’s what I expect will happen this time.”

Grantham called the 2000 and 2008 market declines.

David Einhorn, founder of hedge fund Greenlight Capital

Einhorn said at CNBC’s Delivering Alpha conference that he sees the market doing well in the near-term. But he said there’s no denying how high valuations are, calling today’s environment the “the most expensive market of all time, as far as I can see, at least since I’ve been managing.”

That means that it’s probably not the best time to buy in, he said.

“This is a really, really, really pricey environment, but it doesn’t necessarily make me bearish. Asset prices can trade at the wrong price, and they can trade at the wrong price for a long period of time,” Einhorn said.

He added: “I just observe that it’s a really expensive market that if you buy and hold for a very long period of time, I doubt that this is a great — you’ll look back and say this was a great entry point of all of the entry points that you could have.”

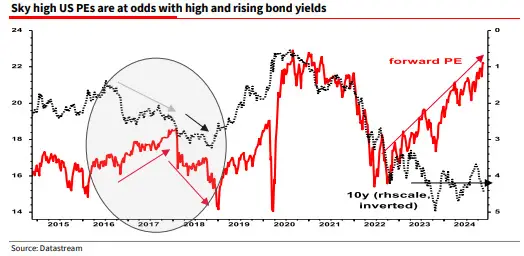

Albert Edwards, the chief global strategist at Societe Generale

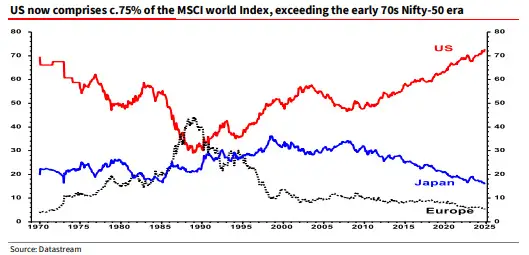

Edwards, who is known for his regularly bearish outlook and calling the dot-com bubble, hasn’t changed his tune. On Thursday, he wrote in a client note that the US stock market capitalization relative to other developed markets has grown to levels seen in prior US market bubbles.

“The dominance of US equity in the global indices (MSCI) has now surpassed the early 1970s extreme,” Edwards said. “And the valuation gap between the US and Europe has never been this stretched. High valuations and eps optimism leave the US equity market vulnerable to ‘bad’ news.”

US stocks’ rising PE ratios are also at odds with rising 10-year Treasury yields, he said.

“Just look at the equity euphoria back in 2018, which initially shrugged off rising bond yields – until they didn’t. The same happened in 2022,” he said. “At some point rising bond yields will just as surely begin to hurt equities.”