‘This looks and feels like the year 2000 to me’: Investing legend Rob Arnott says the stock market’s record rally reminds him of the dot-com bubble peak

Rob Arnott says he’s usually early when calling a bull market top. So when he says the current market environment reminds him a lot of the dot-com bubble peak, it doesn’t mean he thinks a significant pullback is imminent.

It does mean, however, that he sees a big decline somewhere not too far off.

“This looks and feels like the year 2000 to me,” Arnott told B-17 on November 11. “Are we likely to see a bear market in the next two years for large-cap growth? Yeah.”

Arnott’s comments came as the S&P 500 — a large-cap index dominated by mega-cap growth firms known as the Magnificent Seven — jumped 5% within a week following the election of Donald Trump, closing above 6,000 for the first time. The explosive move was the latest advance in a torrid 66% rally that’s lasted more than two years.

A robust economy and excitement about artificial intelligence and business-friendly policies from the future Trump administration have propelled the market to all-time highs. But Arnott believes AI optimism, which has driven the lion’s share of the rally, is already fully priced in.

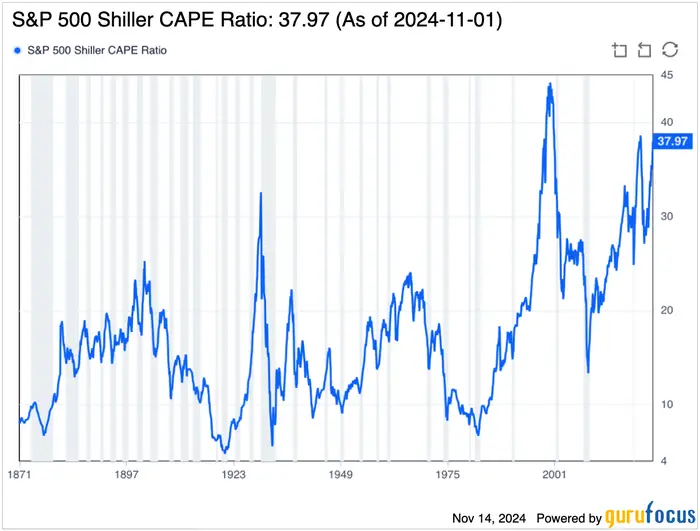

Those high expectations are visible in the S&P 500’s Shiller cyclically adjusted price-to-earnings ratio, Arnott said, which sits at levels that rival the dot-com bubble peak. At 37 times earnings, just below the late-2021 peak of 38, before the market fell by 25%, and the 2000 peak of 43, right in front of a 50% loss.

The problem with high expectations is that the results eventually have to live up to them. But a couple of factors threaten the market’s bullish narrative, he said.

One is that companies like Nvidia will be able to keep their 90% market share as competition rises and the cost of chips eventually comes down.

“If you posed the question five years ago, the presumption would have been that Intel would be the dominant player,” Arnott said. “Well, Intel is teetering perilously close to irrelevance, and Nvidia wasn’t on anyone’s radar screen five years ago. So disruptors get disrupted.”

There’s also the possibility that the pace of AI adoption is slower than expected, Arnott said. He said internet use in 2005 wasn’t all that different from its use in 2000, but that today, things have completely changed. A longer timeline may play out for AI as well, he said.

Arnott joins a long list of strategists and money managers who have recently expressed lackluster outlooks about forward return prospects, given the state of stock valuations.

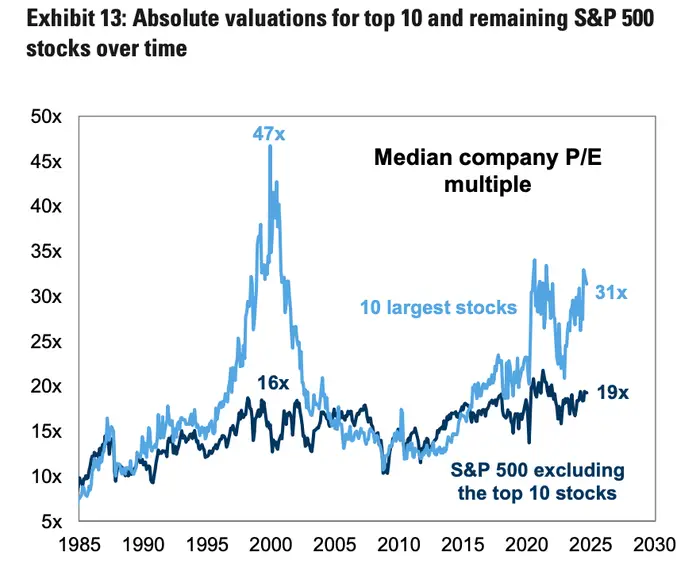

Goldman Sachs’ Chief US Equity Strategist David Kostin made waves in October when he said the S&P 500 would deliver 3% annualized returns over the next 10 years. In an interview with B-17, he also made a similar point to Arnott in that the valuations of some of the market’s most-loved names are much higher than the rest of the pack, similar to what happened during the dot-com bubble.

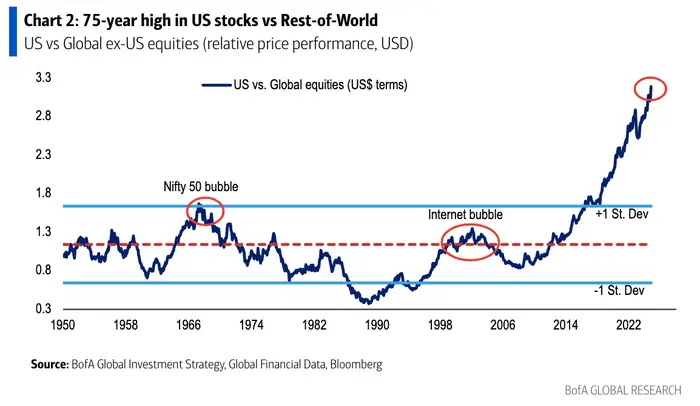

Bank of America’s Global Chief Equity Strategist Michael Hartnett said in a client note on Friday that US stocks have outperformed relative to equities in the rest of the world to the most extreme degree in at least 75 years. Relative performance levels have reached elevated levels in prior asset bubbles like the so-called Nifty Fifty and dot-com peaks.

While Hartnett said it’s difficult to call the top in investor sentiment, the strategist known for his short-winded writing simply said: “sell hubris, buy humiliation.”

Like both Arnott and Hartnett say, it’s hard to call the top. As short-term interest rates fall and the market-friendly policies of the Trump administration on the way, the rally could continue for months or years.

But history shows there will likely eventually be cheaper times to buy into the market, said David Einhorn, founder of hedge fund Greenlight Capital, at CNBC’s Delivering Alpha conference on Wednesday.

“This is a really, really, really pricey environment, but it doesn’t necessarily make me bearish. Asset prices can trade at the wrong price and they can trade at the wrong price for a long period of time,” Einhorn said. “I just observe that it’s a really expensive market that if you buy and hold for a very long period of time, I doubt that this is a great — you’ll look back and say this was a great entry point of all of the entry points that you could have.”

The way Arnott sees things, that better entry point could come in the next couple of years.