This one career mistake may be costing you $300,000 in retirement savings. Here’s how to avoid it.

It’s been proven that those who switch jobs more often make more money over the long term. But there’s one hiccup: your retirement savings rate could fall behind and the opportunity costs could pile up.

A study from Vanguard found that while the median job switcher saw a 10% bump in pay, it coincided with a 0.7% drop in their savings rate. The majority of job switchers (55%) ended up with a decreased allocation to their 401(k) plans.

The study, based on 54,793 workers who switched jobs from 2015 and 2022 between employers that offered Vanguard 401(k) plans, found that the outcome was worse for those who ended up with an employer that offered voluntary enrollment versus an automatic one, and more so for those who only saw a small salary increase or a pay cut.

However, even those who were automatically enrolled, meaning the employer deducted an amount or percentage from the pay for a 401(k) contribution, took on losses, too. The reason is that the most common default savings rate was quite low, at only 3%. And the majority, or about 60%, of new enrollees stuck to that rate, the study found.

How much of a pay increase a job switcher lands is also relevant. Those who saw a raise below 10% saw a drop in their savings rate and the dollar amount they saved. Those lucky enough to snag an increase above 10%, still ended up with a higher dollar amount saved even with a lower savings rate.

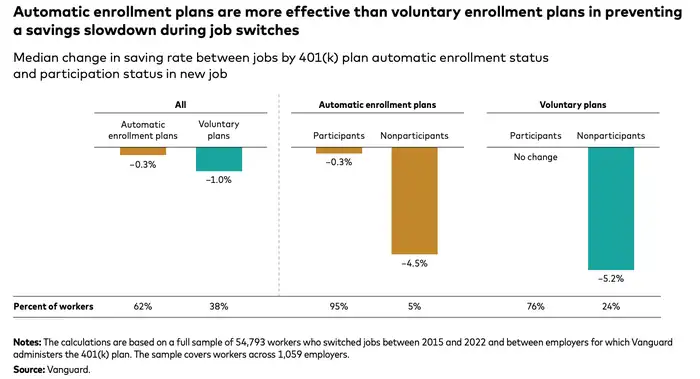

Below is a chart that demonstrates the drop in savings rates based on the enrollment type offered by an employer. Those who moved to an automatic enrollment plan saw a 0.3% drop in their savings rates as opposed to those who moved to a voluntary one, who saw a 1% drop.

If the data isn’t enough to paint a picture, the dollar figure could help quantify it further. The study follows the example of a typical career that involves nine jobs. Using this as a baseline, if you started with a $60,000 salary at the age of 25 and changed your job eight times throughout your career, resetting your savings rate to a 3% default, you could be looking at a $300,000 setback in your overall retirement account by the time you’re 65. It would be equivalent to six years of less spending in your retirement years in comparison to staying at the same job that offered an automatic increased savings rate.

The way out

The study pointed to three main solutions for this problem. For passive savers who are stuck in their ways, it may be up to employers to make the adjustments by increasing the default savings rate. This makes more sense in today’s work culture, where younger workers are more likely to stay at jobs for shorter periods before moving on.

Employers can also set up custom or adjusted savings rates based on an employee’s age, tenure, or years to retirement. For example, the study found that more tenured job switchers who had been in a previous position for longer had the benefit of automatic savings rate increases. Still, upon switching, they saw the steepest pullback in their rate. This is because the default rate drops back down to lower levels.

Another way to do this is by requiring data sharing from the new employee about their previous plan or getting it directly from a shared database, allowing the same rate to roll over.

Now, these are all things that would need big movers and shakers to implement, including policy adjustments. But if you’re reading this, you could take a cue from the findings and remedies by putting matters into your own hands. Going from being a passive saver to an active one, a small habit shift sounds simple, but your future self may thank you as the result could be a six-figure difference. In the example that showed how switching jobs resulted in $300,000 less, an increase from a 3% to a 6% savings rate would reduce that loss to only $40,000.

So, if you’re planning on taking a new role anytime soon or just landed a job, congratulations, now change that savings rate!