‘Time to be patient’: A top fund manager shares why he’s hoarding cash, betting big on gold, and shying away from AI

Jeff Muhlenkamp knows that in some markets, the best way to grow his clients’ money is to do nothing with it.

The manager running the namesake Muhlenkamp Fund (MUHLX) has topped 98% of the funds in the large-cap value category in the last five years, according to Morningstar. He has beaten his benchmark in each of the last four years, and a strong finish to 2024 could extend the streak to five.

What’s fascinating is that Muhlenkamp has outperformed while clinging tightly to cash, even though conventional wisdom says doing so can weigh on returns.

In mid-2022, Muhlenkamp said he had a staggering 45% of his portfolio in cash, which he cut to 30% in early 2023. That unorthodox strategy paid off, as the Muhlenkamp Fund scored a positive return in 2022, which was the worst year for US stocks since 2008.

Although Muhlenkamp has since put cash to work, he still has about 14% of his fund’s assets on the sidelines. Much of that stockpile was built when he trimmed positions that hit his fair-value levels. The leading fund manager is in good company, as Warren Buffett’s Berkshire Hathaway held a record level of cash, which was about 17.5% of its assets, midway through the year.

In a recent interview with B-17, Muhlenkamp said he’s willing to deploy his cash pile. However, he added that the hurdle to invest is unusually high since stock valuations are pricey, the economy seems to be weakening, and cash is yielding around 5%.

“If I find a compelling investment, I’ll put money to work tomorrow,” Muhlenkamp said in a recent interview. “I don’t care what the rest of the world looks like, but there’s just not very many out there. I mean, everybody talks about the FAANGs and the Big Seven and all that stuff, but the whole market is pretty expensive.”

Risks abound, from AI to zig-zagging jobs data

As Muhlenkamp noted, the market’s most popular stocks are mega-cap technology firms. They used to go by the “FAANG” acronym but are now colloquially known as the Magnificent Seven or Big Seven. Many of these stocks have been rewarded for going all in on artificial intelligence.

“They all know that they can’t miss the next big thing,” Muhlenkamp said regarding AI. “They all believe that this is the next big thing, and they all have very deep pockets to go spend the billions and billions and billions of dollars that are required to deploy this next big thing.”

The primary AI company in the crosshairs is Nvidia (NVDA), which had been the market’s hottest stock since demand for its industry-leading chips soared to astronomical heights. However, shares took a substantial hit this summer as investors worried that AI demand would level off if it didn’t translate to immediate returns for tech giants.

“Their customers have not quite yet decided how much they’re willing to pay for the benefits of this next big thing,” Muhlenkamp said. “So all the tech guys are spending their capital, money to build out the capacity, and I think it’s an open question whether they actually get a good return on their investment or not.”

Investors also may have gone overboard about AI, Muhlenkamp said. Nvidia’s generous valuation will only be justified if companies keep scrambling to pay premiums for its AI chips. Otherwise, the company may not claw out of the bear market it’s in anytime soon.

“It’s probably more like Cisco in 2000,” Muhlenkamp said of Nvidia. “Cisco had real orders. I mean, they had the best routers out there, and they had a ridiculous backlog form, and they could upcharge for ’em, and were building out the internet across the world, and then it got built. So now demand drops by a third or a half, and competitors come online with cheaper products.”

Another chief concern for Muhlenkamp is the economy. He estimates that half of the relevant economic indicators are negative and the other half are mixed, including Friday’s jobs report. The US unemployment rate ticked down slightly, and while employers brought on more workers in August than in July, last month’s job creation number still undershot estimates.

While some pundits have all but ruled out a recession, like Steve Eisman of “The Big Short,” Muhlenkamp said he isn’t so sure. The odds of whether the economy contracts are akin to a coin toss, the fund manager said, noting that some sectors are already feeling the pain.

However, Muhlenkamp pointed out that US stocks broadly remain richly valued. The economic expansion could continue, he said, but markets should be accounting better for potential pain.

“There are very, very few companies that are priced as if the market expects a recession — even though manufacturing’s in a recession, trucking industry’s in a recession, the chip industry’s in a recession,” Muhlenkamp said. “Those are all true, but it’s not reflected in prices. Which means: time to be patient.”

A golden opportunity for investors

Even in a market where discounts are scarce, Muhlenkamp has investments where he’d put money to work, including companies connected to gold.

“Gold started hitting these all-time highs, and none of the gold-related stocks were moving at all,” Muhlenkamp said. “I said, ‘Wow, what an opportunity.’ The opportunity is still there.”

The yellow metal has snapped out of a yearslong malaise by rising 22% this year, though Muhlenkamp noted that gold mining stocks like Newmont (NEM) and Royal Gold (RGLD) didn’t catch fire until late March. Those companies, which are now two of Muhlenkamp’s larger holdings, are up 49% and 22% since then, respectively, but he believes they’re still undervalued.

For example, Newmont is trading more than 40% below its all-time high from April 2022, even though gold is near a record of its own. Muhlenkamp doesn’t see a reason for the disconnect.

“Our thinking is always: cheap, hated, and in an uptrend,” Muhlenkamp said of his strategy. “And if you start looking at cheap and hated, that’s usually a good place to start looking for good prices on companies.”

Gold isn’t just a stronghold against a weaker economy — it’s also a time-tested hedge against higher inflation. Muhlenkamp fears that inflation could reaccelerate to 3% or 4% going forward since government spending is much higher than what he’s comfortable with.

“You are devaluing the currency against real things — real, tangible things,” Muhlenkamp said. “Whether that’s crude oil, whether that’s gold, whether that’s a house, it takes more greenbacks to go buy the same darn thing.”

Unlike Eisman, Muhlenkamp has serious doubts about the US dollar, which is why he said his allocation to gold-related investments is 7% to 8% — the highest it’s ever been. Based on his enviable track record, investors may want to follow suit.

“You’re getting a lot more traction in terms of actually using gold as a currency, things that we haven’t seen in, what, 70 years?” Muhlenkamp said. “I’m not predicting that that continues to happen, but if it does continue to happen, then I think the price of gold will move up very nicely. And that gives a nice risk-reward there for companies that have exposure to the price of gold.”

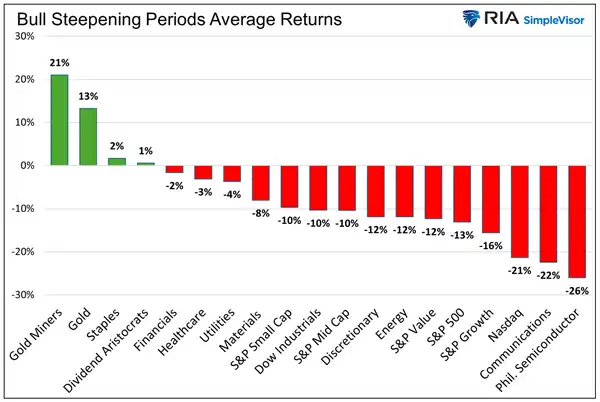

Muhlenkamp isn’t alone with this call. Michael Lebowitz of RIA Advisors noted this week that gold and gold-mining stocks have historically dominated in so-called “bull steepening” periods where softer economic growth and lower inflation lead the Federal Reserve to cut interest rates, as is almost certain to happen this month.