Welcome to credit card points mania

When played right, credit card rewards can unlock a world of luxury. But it comes at a cost.

Aaryan Desai picked up a hobby during quarantine: researching credit card rewards.

The 20-year-old swipes as much as he can. Right now he’s banking points for a concert in October and a big trip after he graduates from Georgia Tech.

Desai is part of a new generation of credit card users: young, perks-focused, and ready to maximize. Today’s credit cards, he said, are like the coupon books of yore. The perks might not always be the right fit, but, if you figure out a good configuration, you can find some big savings.

For Desai and other rewards hounds, the realization that they can perform a sort of points arbitrage was a real hook.

“Just using the money that I would be using otherwise or just getting together with friends and that, ‘hey, I can just put it on my card and you can Venmo me later,’ opening the door to getting 80,000 points from Chase or 175,000 from American Express — it was a new opportunity,” he said, adding: “That’s what got me into it.”

If it seems like the whole country suddenly has credit card point mania, you would be correct: An Ipsos poll of 1,081 adults conducted from April 31 to May 1 found that 71% of respondents have a rewards or cashback credit card, and 68% said that they prefer using their credit card because of the rewards and points that they can earn.

The poll found that a fifth of Americans ages 18 to 34 use their rewards to pay for things they wouldn’t be able to afford otherwise. Younger Americans are flocking to previously fancy cards like American Express, willing to shell out hefty annual fees in exchange for perks like exclusive access to Coachella tickets.

The rewards are a big reason credit cards have become a cultural juggernaut among young Americans. As costs rise and the millennial subsidy fades, credit card rewards help a new generation live lifestyles they may not otherwise be able to afford: first-class flights, hotel rooms, and VIP concert experiences. It doesn’t hurt that social media is full of videos and blogs that offer the tantalizing promise of free trips, luxury lounges, and fancy restaurants — if you can cobble together the right puzzle of points and cards without digging yourself into too much debt.

Living the high life on credit card perks

At first, 29-year-old Willem Van Eck thought the rewards game was a snake oil salesman’s gambit. Cut to: He’s stretched out in a first-class seat, a glass of bubbly in hand.

“Wow,” he thought, “this actually is a scheme that you can leverage with the right flexibility and with the right research,” Van Eck, a software engineer in the Bay Area, said.

Credit card rewards work as an incentive to get customers to swipe more. They can come in the form of cashback — which means you get a partial refund for a given purchase in the form of a credit on your bill or a transfer to another account. Or they come as points, which are more nebulous but can typically be used as currency for future purchases. And then there are other perks like hotel credits, airline miles, gift cards, and upgrades like Van Eck’s.

For instance, the Platinum Card from American Express — often considered one of the top cards for rewards — will cost you $695 in annual fees. In return, you’ll get five points for every dollar spent on flights and a point for every other dollar spent. On average, per B-17’s calculations, an Amex point is worth 1.8 cents. Say you spend $5,000, $2,500 of which went toward flights; you’d net 15,000 points, which could equal around $270 — a significant chunk of the annual fee.

In addition, many cards will also offer substantial sign-up rewards. The Platinum Card offers 80,000 points for spending $8,000 in the first six months of holding the card. Those 80,000 points alone could be worth twice as much as the annual fee.

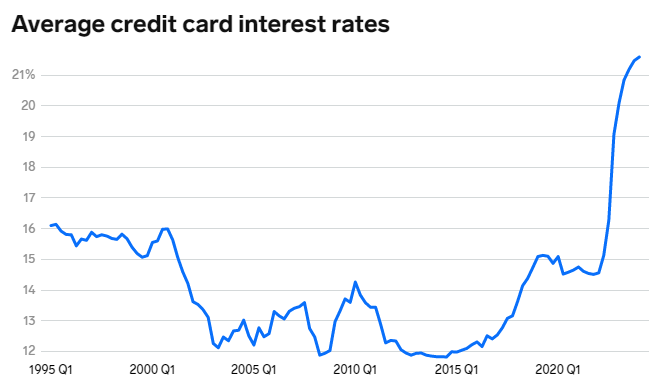

Taking advantage of this system requires diligence and restraint to avoid paying more in interest and fees than you gain in rewards. According to a paper looking at who this system hurts and benefits, borrowers who carry balances and businesses — which pay a fee on each credit card transaction — subsidize the fun for the rest of us.

Pre-pandemic, Van Eck was chasing cards with high sign-up bonuses, like the Chase Sapphire Preferred card, because they allowed him to transfer points to airlines so he could book business or first-class seats. During the pandemic, he took note of the beefed-up bonuses and short-term benefits that companies were offering in an attempt to lure customers; his Delta card offered a $15-a-month dining credit, for instance. That’s when Van Eck noticed that more of his Gen Z and millennial friends starting to become adept at navigating their benefits.

Van Eck is very cautious of lifestyle creep and ensuring that cards are worth his while, especially amid high interest rates, inflation, and recessionary fears.

“I’ve seen most of my peers, including me, reevaluate the value proposition of the cards,” he said. Every year, he goes through his list of cards to see which ones paid for themselves without him changing his behavior. If one doesn’t, he’ll cancel it.

But not everyone is as prudent as Van Eck. In the high-paying tech industry where he works, Van Eck still sees people changing their habits to maximize rewards, which he doesn’t think is smart.

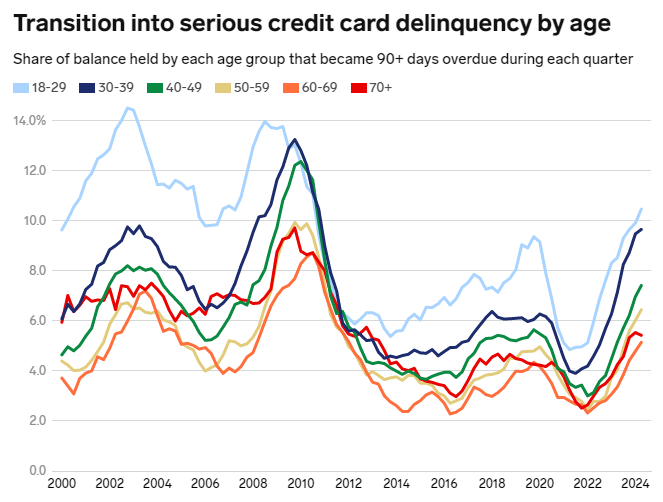

This could be why delinquencies have been on the rise in recent years, with the youngest borrowers leading the pack. After all, credit cards are fun to use. No, really. Contrary to the belief that we overconsume with credit cards because they ease the pain of spending, research finds that their bigger appeal is that they make our brains feel like we’re getting a reward. All that stands between you and access to that first-class airport lounge are a few taps or swipes.

Nothing good lasts

Credit card companies aren’t just giving away rewards for free.

As Lulu Wang, an assistant professor of finance at Northwestern’s Kellogg School of Management finds, many businesses will pass on their costs to customers. For example, say you use a 1% cash back rewards credit card at your favorite local coffee shop on $100 worth of coffee for you and your friends. The shop pays a 2% fee on the transaction — $2 — to your card issuer. Then, your card issuer would use some of that 2% fee to give you your 1% back. To cover their fee, the shop might raise their prices.

“In some sense, when you benefit from those rewards, you’re taking that money from some mix of the merchant and other cash and debit card consumers out there in the economy who are then not benefiting from those rewards,” Wang said.

Perks aren’t always a great deal for everyone. Will Springer, a 41-year-old in Indiana, uses his Chase Sapphire Preferred and Amex Platinum cards primarily for perks like travel insurance and car rentals. Since he lives in a more rural area, an Equinox gym membership benefit is moot, and he can’t really use the Uber benefit offered — he sometimes converts it into food delivery credit for Uber Eats.

Other loyal credit card point users say you can’t bank on your favorite perks sticking around. Brandon Zemel, a 32-year-old music producer in Las Vegas, puts pretty much everything on a credit card. He has two cards, the Chase Sapphire Reserved with a higher annual fee that’s more travel-catered, and the Chase Freedom Unlimited, which has a fairly flat return on points. He said his travel card shaves hundreds of dollars off of his expenses, and he loves to use his points to get himself onto seat upgrade lists.

But Zemel recently lost a hugely useful travel benefit: a “priority pass” that could be converted into a $28 dining credit for both him and a guest.

“It seems to be a thing these days that every year, two years, three years, these companies devalue their product or their perks provided by their product,” Zemel said. “And I guess to some extent it’s to be expected, but it does kind of remind you that the things that you currently enjoy are not necessarily going to be here long term.”

As Zemel has seen during his time as a cardholder, the rewards craze has basically “grown exponentially,” propelled by popular blogs and TikTokers. That can also dim the appeal of previously exclusive perks, like overcrowded airport lounges.

“People got really used to anyone with a pulse basically having some kind of access to the lounge at the airports,” he said. Now, Delta has recognized that it had too many elite cardholders — leading it, in some cases, to restrict access to lounges to higher spenders.

It’s what Wang says is an example of “skyboxification” — an increasing stratification of life among haves and have-nots, like a baseball stadium that’s divided between crowds in the stands and richer fans in box seats.

“I can totally understand this looming dread that society is getting splintered into those who have access to this kind of stuff and those who don’t,” Wang said.

I can relate to this sentiment. At a music festival this summer, I learned that my Chase Sapphire credit card would let me skip the line and access an air-conditioned tent with free water.

However, when I arrived I learned a hard truth: I actually needed the card one tier above mine to get in. For one brief moment, as I gazed at the sparse crowd inside, I thought about applying on the spot. But I ultimately decided it wasn’t in my best interest to incur a higher annual fee and open another line of credit.

And yet, as I stood among the packed and sweaty masses, waiting nearly an hour to get food and water, I felt haunted by the skybox appeal. Would a new credit card do anything positive for my finances? Most likely not. Would it make me feel like a VIP at this event? Definitely. Maybe I’ll try to get the Sapphire Reserve before next year’s festival.