Apollo just set a goal to manage $1.2 trillion in private loans by 2029. These 7 slides show how it will get there.

Marc Rowan, CEO of Apollo

The biggest player in non-bank loans has set a massive new goal for itself: more than doubling its $562 billion private lending business to $1.2 trillion in five years.

The trillion-dollar goal has become a high watermark for asset managers generally. Blackstone became the first private-equity firm to manage $1 trillion in assets last year, while KKR set its own trillion-dollar goal this year.

But unlike its competitors, Apollo gets the lion’s share of its growth comes from its lending arm, which was bolstered by growing demand for private credit in the face of a banking crisis, and by the firm’s merger with retirement services provider Athene, which has provided Apollo with the ample capital it needs to make loans.

“Everywhere in the world, banks are being asked to do less, and investors are being asked to do more,” Apollo CEO Rowan said at the bank’s annual presentation for investors on Tuesday.

Indeed, private lenders like Apollo are increasingly providing investment-grade lending to large corporate clients in addition to short-term loans. On Tuesday, Rowan and Apollo’s deputy CIO of credit, John Zito, pointed to Apollo’s AB InBev deal four years ago as a watershed moment for the firm, and a told-you-so moment for the industry.

“When we did the first investment grade financing for AB InBev a number of years ago, many in this room and many of our competitors and most of the street said, ‘That $4 billion is the last $4 billion that you will ever do,'” Rowan said. “That was $100 billion ago and $11 billion just for Intel. This is just getting started.”

At $1.2 trillion, Apollo will manage as much in loans as JPMorgan Chase last year, according to data tracker Statista. (Rowan and JPMorgan CEO Jamie Dimon have debated the merits of private credit before, as B-17 has previously reported.)

Apollo plans to more than double both its private credit and equity businesses by 2029, which would bring total assets under management to roughly $1.5 trillion. At its last investor day in 2023, it set a goal to hit $1 trillion in total assets under management, including private loans, by 2026.

Here’s how Apollo plans to grow to over $1 trillion in private lending alone.

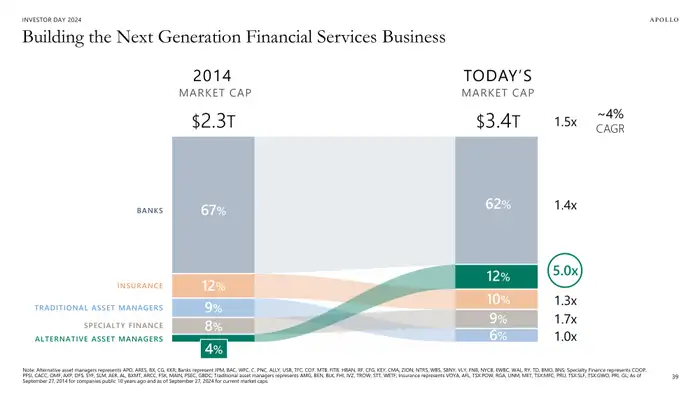

Financial services as a whole have grown by 50% over the last ten years. Alternative asset managers have grown 500%.

Asset managers have grown their market cap five times in the last ten years.

Alternative asset managers like Apollo and Blackstone have been the stars of the last ten years in financial services. The industry’s market cap has grown from $2.3 trillion to $3.4 trillion since 2014, but alternative asset manager’s market caps have grown from only 4% of all financial services to 12%, and they’ve grown five times over in ten-years.

Rowan looked back to 2008, when all of the largest alternative managers were roughly $40 billon in assets under management. By the end of 2023, when the firm was at $650 billion, it had grown between 16 or 17 times over, numbers that Rowan said are rare in financial services.

“We actually outgrew Apple, we outgrew Microsoft, ” Rowan said. “We outgrew almost every growth company you could think of.”

The capital needs of the future are long-term and complex.

According to Apollo, we are entering a new financial era.

Apollo forecasts up to $100 trillion in capital expenditures in three interconnected growth areas over the next 10 years: $30 trillion to $50 trillion in energy transition, $30 trillion in power and utilities, and $15 trillion to $20 trillion in digital infrastructure like data centers.

But while banks and the capital markets fueled the last great era of growth amidst low interest rates and globalization, the firm thinks that this “new era” may look like a much older era, 1890 to 1920.

“We’ve seen this movie before,” James Zelter, copresident of Apollo Asset Management said. Insurance companies, like New York Life, were the main sources of the capital necessary to finance the infrastructure of a new era, such as railroads and electrification.

“The capital needs were long-dated at that point in time,” Zelter said. With a new turn towards a new era of infrastructure, capital needs have again become much longer than the balance sheets of the banks, or the public capital markets, can handle.

Apollo’s ability to originate many different forms of capital is a differentiator.

This slide compares Apollo Credit’s lending capabilities with traditional lenders.

Apollo’s merger with Athene brought life insurance and retirement capital to its balance sheet and is a key part of Apollo’s future strategy. Athene’s balance sheet has $235 billion in assets under management, plus an additional $69 billion from its Apollo-Athene dedicated investment program, and an additional $392 billion in third-party capital from clients.

That capital, especially Athene’s capital, which needs to pay out life-insurance annuities, is looking for long-term, safe yield. While many alternative firms are working with life-insurance capital, Apollo has brought it in-house. This allows the firm to lend in a wide-variety of ways over the long-term.

As banks scale back their own lending, Apollo expects to step in and finance the future.

“These long-term solutions across a variety of cost of capital are not really appropriate for bank balance sheets who fund themselves short,” Rowan said.

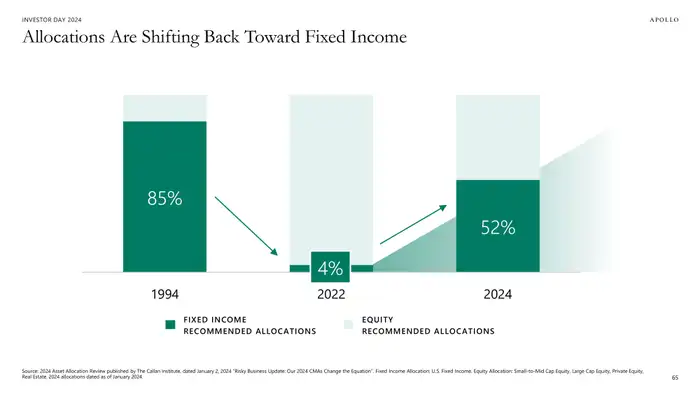

Allocations towards fixed-income are up, providing a runway for the firm.

This slide shows that allocations to fixed-income are back up to 52% this year after falling to as low as 4% in 2022.

Apollo has its own capital to invest, but it also of course invests on behalf of other investors. And through that activity, it sees allocations to fixed-income and debt, rising, the firm’s executives said on Tuesday.

“If you showed me the page from 1994 to 2022 and this is the allocation of fixed income, I would have told you it would be a horrific career decision to be in fixed income from 1994 to 2022,” Zito said. “We built our business as everybody was taking money out of fixed income.”

Still, the firm grew multiple fixed-income business lines, which now should give it a head start and help attract investors.

“There are many of our competitors who literally do not have a credit allocation team because they got completely out of the business,” Zito said. “They’re just starting to build the business back up.”

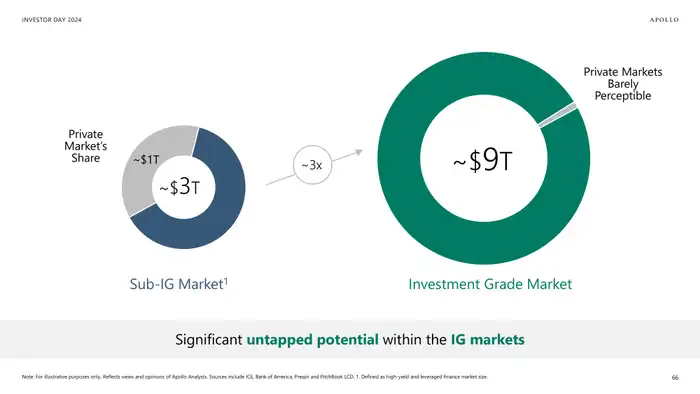

Apollo sees growth in the investment-grade market…

This slide shows how the private-market has started to penetrate the sub-investment grade market, but not the investment-grade one.

The private market has made a large impact on the sub-investment grade market over the past ten years, taking up $1 trillion of the roughly $3 trillion market. But it’s barely even tapped the surface of the $9 trillion investment-grade market, of which Apollo is a clear leader with its Intel and AB InBev deals.

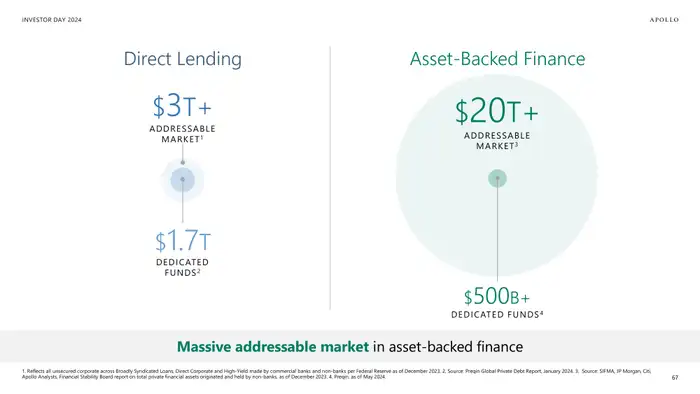

… and in asset-backed finance.

This slide shows how private-firms have made an impact on direct-lending, but still have a long runway in asset-backed finance.

Additionally, there’s a $20 trillion asset-backed finance market with only $500 billion in funds raised, a pittance.

“In asset-backed, no one’s really done it,” Zito said. “It’s very small. We think it’s one of the biggest drivers of our business over the next decade.”

Origination is key, but the firm is still a money manager.

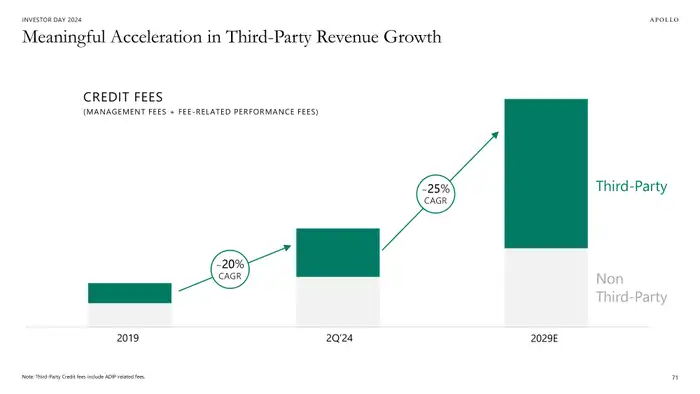

Apollo still plans to make a lot of its fee-revenue from managing third-party capital.

While Apollo’s Athene transaction brought huge amounts of capital to its balance sheet, the firm was quick to silence any naysayers who said that was the firm’s only large growth bucket.

“Many people look at our growth and they’ll always say, okay, it’s driven by Athene, not third party.” Zito said. “You’re seeing we grew third-party revenues in the last five years by 20%. The next five years, we anticipate third-party revenues to grow by 25%.”

While Apollo plans to explore new frontiers over the next five years, it definitely hasn’t forgotten its original DNA of making returns for its third-party investors.